Brookfield 2Q24 | Economic Value | AI and Cloud

Today’s quote is buried down in the post. Happy hunting!

~15-20 min read

3 Things Before we Start:

1: Welcome to Brookfield, Mr. Ackman:

(Ackman’s a pretty good value investor.)

Clearly he’s been reading my posts. Clearly. *chest thumping noises*

That means I’m good, too, right? Because we found the same idea?! Nah. It just means we both go down in the same ship if wrong. (I don’t think we are.)

2: I edited our recent update on KKR for clarity.

Mainly, I cleaned up or added examples/explanations of how recent activities and results were changing the business. E.g., I re-wrote the explanation of how GA is now exploiting KKR’s client relationships to raise capital to underwrite new insurance, effectively selling KKR’s client’s a “new asset class”: blocks of insurance.1 That allows GA to grow without using its own capital to do so, instead only charging a fee. In the process, this may also improve GA’s returns on capital. Win-win for KKR.

3: I’m working on new stock ideas.

I found several recently and have been kicking the tires. I already bought a 5-6% position in one2, sourcing funds from Berkshire, Bank of America, and DaVita. I just have to write it up. Spoiler alert: it’s a bank. Haha, you thought it was going to be be a cool company? Wrong Substack page!

Ah heck… here… the stock is Citigroup and I think you’ll find it cool in a nerdy way.

First, it’s an interesting turnaround situation. Most turnarounds turn out to be attempted turnarounds that investors call “value traps”. Citi had tried restructurings and other things under Michael Corbat (2012-2020), never quite getting there and only earning an ~11% ROE at the '18-'19 peak, which, for a bank, is not good.

Under Jane Fraser, it really does look different. I was not a believer after I watched their 2022 investor day and other presentations. But I follow all major US banks because of our bank investments. At Citi, there are now loads of tangible results and I would have been irrationally stubborn not to take a second look at this evidence and re-evaluate. I ran some numbers and found the stock is still wildly disconnected from intrinsic value even if Frasers’ plan only half-works while we also go through a recession. Furthermore, talented senior executives have joined Citi from JPMorgan and Bank of America — the industry’s best. E.g., the guy who now runs Wealth at Citi is the same one that turned Bank of America Merrill Lynch into an absolute powerhouse of an investment advisory business (who we must thank as BAC shareholders). They wouldn’t be doing this if they didn’t see a cultural fit, and saw Citi going from mediocre-to-good. To go from a great bank with a great future to a mediocre bank with no future would be a bad move, so I think they see what I see.

We’re buying mid-turn. Although the stock’s ripped some and we’re 50% late for the party, I believe the odds have shortened significantly, the outcomes are more certain, and yet the risk/reward is still exceptional with very strong protection of our capital.

I think you might enjoy the Citi write-up. The banks we’ve covered and owned so far are more consumer and small business oriented. Citi’s more involved in the financial industry’s plumbing and the supply chains of multinational corporate clients, so you’ll get more of a behind-the-scenes look at international finance.

I have a half-written update on DaVita but will probably leave it until 3Q while I focus on new stocks (and write them up for us!).

Brookfield’s 2Q24 Earnings

(REMINDER: Everything below, including share prices/values, are USD unless noted. Brookfield reports and functions in USD though it’s Canadian.)

If you first need a short refresher on my Brookfield/KKR/industry thesis, find it in the recent KKR update. See the recent KKR 2Q24 update for context on the economic backdrop (market valuations, interest rates) affecting the industry if you’d like. I won’t restate it here and will touch on different things instead.

We’ll go through things the usual way, highlighting (a) progress on the business’ KPIs, (b) qualitative changes and relevant industry info, and finally (c) where we are on valuation and any relevant portfolio decisions or considerations. That’ll be interspersed with some business/investing insights, possibly memes.

Here we go!

Brookfield Asset Management (BAM) is doing well, though revenues are lagging. Fees are up only 5% y/y, much less than peers, which if I had to guess is why BAM fell 4% on the earnings date. This looks short-term, as (a) there are levers for BAM to pull and (b) the industry backdrop is improving.

Fundraising, AUM, fees: BAM raised $68 billion in 2Q and $140 billion in the last 12 months (LTM), and fee-paying AUM is up 17%. Of this, $49 billion is from BN’s acquisition of annuity/life insurer AEL, implying fundraising has been a bit slow recently, and client fee-paying AUM grew only 11%.

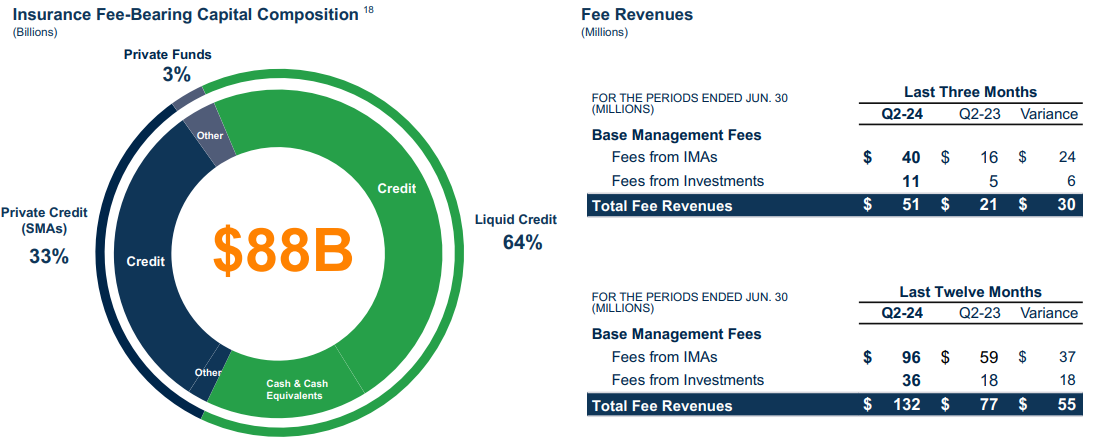

Fee growth will catch up as BAM brings AEL’s portfolio under its umbrella.3 Economically, it looks like the charts below. I’ll explain it.

Between AEL and insurance businesses BN already owns (via BNRE / Wealth Solutions4), BN had $88 billion of fee-bearing AUM for BAM to run. 64% is still invested in cash and corporate bonds, most of which will be rotated into BAM’s private credit funds (some will be kept as is for liquidity).

So, that 64% will decline to perhaps ~20-35% and BAM will get a ~0.25% fee on it.

Once in BAM funds ~75% of that $88 billion will earn a ~0.9% fee (say). That gets us 0.25% * 25% * $88,000 million + 0.9% * 75% * $88,000 = $55 + 600 million = $655 million in fee revenue. That’s ~$500 million more than $132 million BAM got from BNRE LTM, as shown in the bottom right side of the image above. BAM earned $4.5 billion in fees LTM, so that’s a ~12% growth tailwind (~500 / 4,500) next ~2 years, or ~6% growth annually. BAM just needs to deploy AUM already contracted to it.

That revenue should have a >60% incremental operating margin since BAM already hired the investment professionals it needs to put the money to work. That compares to the ~56% margin BAM’s earning today, which is depressed partly for this reason. In turn, that implies a >6 percentage point contribution to profit growth annually from this insurance tailwind alone.

BNRE is also underwriting ~$24 billion of new business annually. That’ll add another 4% to BAM’s fee growth, calculated in this footnote5, and >4% to profit growth. So BNRE alone gets BAM >10%/yr profit growth over the next 2 years.

None of this has to do with the >10% industry AUM growth that leaders like BAM are getting from external clients, adding more fuel to the fire. In 2025-2026, BAM will be raising flagship infrastructure, infrastructure debt, private equity, real estate, and private credit funds, which should accelerate fundraising beyond its recent $20-30 billion/qtr6.

BAM is also limiting client inflows into some products. It’s first been adding capacity to ensure it can deploy the capital at attractive rates of return:

“in our retail wealth products, I would say this is one component of our business where we are actually limiting our fundraising based on the deployment. And as we deploy more capital, we're going to see much more significant fund inflows into our retail channel as well” — Connor Teskey, Partner, President, BAM

This also points to pent-up growth.

So yes, BAM grew fees only 5% year-over-year this quarter. Yet, given the above, it’s reasonable to expect significantly higher fee and profit growth (well above 10%) going forward 2-3 years. Management thinks 20%/yr nearer term. This doesn’t seem farfetched.

Performance & carry: Not much has changed and I see no reason to change my recent carried interest assumptions or valuation.

(As if calculating carried interest isn’t complicated enough, there’s more to it at BAM/BN because the two split the carry7. I value the carry attributable to BN as a single series of cash flows regardless of where it comes from.)

Carry-eligible AUM is $232 billion, up 6% from $219 last year. Fund performance at industry leaders like BAM improved recently on the back of better market conditions. Industry deal activity is up significantly, allowing Brookfield to “realize” more of its investments and convert accrued carry into cash flow. It’s also been able to refinance $75 billion of debt, at credit spreads 55bps (basis points; 100 basis points = 1 percentage point) lower than the previous debt, which also indicates a more active market. Qualitatively, “bid-ask spreads”, the difference between where the sellers want to sell and the buyers want to buy, have also been coming down as private-equity-owned companies absorb higher interest costs.

With the exception of a recent real estate fund vintage, BAM’s funds are doing well for clients, and BAM has done well for clients through economic cycles. Every quarter, Brookfield lays it on thick and consistently with respect to its investment process and discipline, and regularly highlights deals that fit its capabilities.8

Although we can’t predict market conditions next 1-3 years, things look good for now. We we’re going to get our carry, we just can’t be certain of the timing.

That’s it for BAM.

Insurance (BNRE): after BAM takes its fees, BNRE earns the remaining “spread” on the insurance book of business (investment portfolio returns minus payments to insurance policyholders, explained in this footnote9).

BNRE’s spread-based earnings are ~flat quarter-over-quarter at a $1.4 billion run-rate, but will march toward BN’s $2 billion target over 2-3 years as BAM rotates BNRE’s portfolio out of legacy corporate bonds into BAM’s credit funds. The numbers imply BNRE’s going to exceed its target returns on equity and may do 18-20%+.

BNRE’s now writing ~$2 billion of new business monthly (~$24 annually). These insurers operate with 8-10x assets/equity, so BNRE will retain the entire $2 billion stream it earns to grow at this clip. Since BNRE’s already earning ~16% on equity and rising, this is a great use of capital for us. If they dividend us that $2 billion instead, would you be able to earn 18% with it, in a moderate risk platform that’s already built out, in a slow-changing and long-proven-out industry and business model? Exactly.

(These are the drivers of intrinsic value right here. We’ll write and math it out in detail one day, but I’m talking to you, right now, directly in terms of those drivers: growth, returns on capital, the implied reinvestment rate [g / ROIC] or profit retention rate, and the cost of capital. More in this footnote if you like.10

In the 2002 Berkshire meeting — when I was in Grade 9 and didn’t know this stuff — Buffett was asked about why banks traded at far lower multiples than the S&P 500 at the time. Buffett waves his hand and says he wouldn’t look at businesses this way. He states if you really wanted to compare which is cheaper, you’d have to think about the individual business and what incremental return it will earn on equity — on incremental equity, and for how long. You’d then compare to what you think about the S&P 500 if you aggregated the underlying businesses and thought about its return on incremental equity. A lower multiple doesn’t mean a business is cheaper than the index or not, and it doesn’t mean the business is cheap on its own or not. Ultimately, multiples come from the drivers of intrinsic value. Those things are growth, returns on capital, the reinvestment rate, and the cost of capital. It’s clear when he says “incremental return on incremental equity” that he’s thinking about returns, growth, and reinvestment. He had this framework in mind and pulled it out to answer the question in a robust, “first principles” way of thinking. He points out money “all spends the same” regardless of the name of the company it comes from, so as an investor your only job is to think about the economic characteristics of the business that go into producing those cash flows.)

I mean, if you have a company that earns 2% on capital is retaining its profits and reinvesting hard to grow and maintain its market position, but you think you could otherwise earn 10% on capital elsewhere… then what you’ve got is… well… a huge waste of time and money.)

Look again at BNRE. The business has prospects of earning at least 15%, and potentially 20% on incremental equity. And it’s retaining 100% of its $2 billion in forward profits and plowing them back into the business at those rates of return. If management continues to execute well and the company is able to eventually garner a large share of the annuity market, that’s going to keep happening. Individual annuities are a $2.6T market in the US alone, to say nothing of of the $13T group annuity market (pensions), which BNRE also participates in. BNRE’s only got a $100 billion balance sheet so far.

It could not be more evident this thing may create significant economic value, and could very well be a home run for BN.

Other balance sheet holdings:

BPG: property valuations appreciated in the quarter, a good sign. Rents in BPG’s “core” assets are also at record levels. Occupancy ticked down but is noise. Triangulating with third-party data points like the fact there’s little new office construction and high-teens vacancies (a generational high) in key cities like NYC where BPG’s got big investments, it seems like BPG’s office portfolio has stabilized.

As rents rise, you’d expect cash flows to start growing again even if interest rates stayed high.

Although I trust management, there’s frankly less BPG disclosure than I’d like given the office real estate situation. I’m maintaining my base case and downside case write-downs on BPG. Because of our fat margin of safety11, this is still a winning investment irrespective of what happens to BPG. BN’s got $11 per share in offices, and there was a boatload more upside than $11 from my low-$30s cost basis. The value’s in the $56-83 range.

BN is holding BPG’s “core” assets and trying to sell its “transition and development” (T&D) assets, which are basically buy-fix-sell investments akin to private equity. It sold a bunch before interest rates rose, and then we got stuck with what’s still left when Office Armageddon happened and office transactions froze up. I estimate BPG has sold only 3/90 of its remaining T&D offices, and 3/90 of its T&D malls since 2Q23.

BIP/BEP/BBU: Going to skip this this quarter. Their contribution to BN’s value is low. Cash flow at all these entities is improving, though. They’re all invested in deals alongside BAM’s clients, so if you believe BAM can earn good returns for clients, then you believe BIP/BEP/BBU will benefit. If you don’t, you don’t. I do.

Conclusion:

We just updated our BN valuation in June and got $56-83 as the range of upsides and $37 in downside. Management thinks BN is worth $84. The thesis is largely the same. The company is pulling the levers available to it to exploit the huge AUM opportunity and dealmaking opportunities in front of it, while maintaining its disciplined, value investment approach.

I’m considering trimming other stuff and adding to BN, since the risk/reward again looks good, and better than other positions like Berkshire. I’m buying a business that’s just as good, if not better, and which I understand better.

BONUS: Brookfield, AI, and cloud computing:

Brookfield’s investment circle of competence is “businesses that make up the backbone of the economy.” These are capital-intensive businesses performing mission-critical economic functions. That’s renewable power. That’s real estate. That’s cell towers. That’s rail & toll roads, ports, and container shipping.

In cloud & AI, you know Microsoft Azure, Amazon Web Services, and Google Public Cloud, the “hyperscalers” who provide the software and the IT infrastructure. You know NVIDIA, who has a near-monopoly on the chips best suited for training AI. You might know Micron, who makes memory chips for the servers. But there’s way more to the huge value chain that brings this all about.

You may not think it, but Brookfield sits in the capital-intensive part of the AI and cloud computing investment cycle.

Electricity: electricity is the hyperscalers’ largest operating cost. And they all want to be carbon neutral. And… Brookfield is (I believe) the single largest renewable energy investor in the world. Electricity demand in many developed countries has been flattish for years, but may begin growing. This is the case in the United States, where ~40% of the world’s data center investment is taking place. (It’s putting such a strain on power that it’s no longer feasible to shutter coal mines for the time being. If I had to guess, this is part of Mohnish Pabrai on coal-producer stocks like AMR.) Even if electricity volume demand doesn’t grow, the “energy transition” from fossil fuel plants to renewable power is still well underway, and still needs many, many billions in investment. Brookfield will be doing deals in this huge market for 20 years.

The data center: Brookfield’s also one of the largest data center investors, and has been for years. Data center real estate is specialized (like a hospital) and costs quite a bit. After the IT infrastructure the hyperscalers buy, building out the real estate is the next biggest cost.

The hyperscalers only own the IT infrastructure, the servers and such, and the proprietary software that they’re renting to their customers. They don’t own power generation, and they don’t own the real estate. They rent it.

So the opportunity doesn’t stop at Brookfield’s $10 billion deal with Microsoft Azure. This market is in the hundreds of billions and growing. A single data center requires on average the same amount of power as 80,000 homes.

Furthermore, hyperscalers procure the real estate and the power separately. But it could converge. Brookfield is one of few companies in the world positioned to offer a “turnkey” solution that includes building and renting both the real estate and the power generation. All Microsoft has to do is show up with servers and software and plug them in. In many cases, reliable renewable energy is in shorter supply than data center landlords, so by combining the two into one contract, Brookfield could perhaps extract value by upselling the harder-to-get thing to the guys who need to stay carbon neutral. And a commercial real estate landlord isn’t going to be able to copy Brookfield, because they don’t know anything about the renewable power business.

Economically, this stuff is also not like your monthly electricity bill. It comes under lovely long-term (10-25 year) Power Purchase Agreement contracts with fixed prices and inflationary price escalators, which Brookfield can partly finance with lower-cost debt (partly because of its reputation and scale, and partly because of the revenue and profit stability that those contracts demonstrate to project lenders).

We’ll see how big this gets for Brookfield.

(You thought I was just a stodgy old-school value investor who doesn’t know anything about technology, huh?)

Chris

lol

Sometimes I buy mid-research because I already like what I see so much. Sorry, I never said you get to front-run me! Common Shares is free and I’m not your fiduciary! Everything here is for information! I’m not your fiduciary! I don’t owe anybody timely advice! I may reconsider some of this only if/when it becomes a paid service!)

That’s the insurer’s balance sheet. It’s the money AEL gets from policyholders paying their premiums, which it then needs to invest to earn a higher return than what it’s going to be paying those policyholders on their annuities and such. That money gets managed by BAM under an Investment Management Agreement, where BAM takes 0.25% of all the assets, and then invests it into BAM funds over time, in turn earning the additional fees and carried interest that the funds themselves earn. (I am not sure whether it then nets out the 0.25% against the funds’ fee rates to avoid what might look like double-counting.)

They seem to call it something a bit different every quarter lately and haven’t quite settled on a name.

$24,000 AUM * (655/88,000 revenue rate) / 4,500 existing revenue = 3.96%. The 655 million is the built-up estimate of what BAM would earn on a portfolio of BNRE’s investments that you saw us make a couple paragraphs earlier. The 88,000 million is the total size of that investment portfolio it would earn our estimated 655 million on. 4,500 is BAM’s existing revenue run rate.

This is excluding the $49 billion AEL acquisition. BAM raised $140 billion LTM AUM, minus $49 billion = ~$90/yr = ~$23/qtr

BAM gets two thirds of all its future funds’ carry, while BN gets one third. BN then owns almost 75% of BAM, and therefore eventually gets the carry-based-earnings from BAM’s dividends and reinvestment. In effect, BN therefore gets 83% of the carry on Brookfield funds. BN gets all the carry on older funds. Better yet, BAM or BN (I can’t even remember at this point because it’s not important enough) gets only 50% of the carry from Oaktree funds, and Oaktree’s senior principals (from before the Oaktree acquisition) get the other half. On Brookfield funds, Brookfield entities get 70% and employees get 30%.

E.g., investments involving both data centers and renewable power, wherein plenty of investors can do deals involving one of these, but almost nobody can do a deal involving both, which is probably why Microsoft chose to ink a $10 billion deal with Brookfield and not someone else.

That’s the net investment returns on BNRE’s assets minus the cost of policyholder liabilities, which accrues to us at BN. The spread works just like the net interest income we’ve talked about at banks many times, since that is also an interest spread. That’s where a bank basically takes depositors’ money and invests it into loans. The loan assets then “yield” some rate of interest, from which you subtract the interest on depositor liabilities, and what’s left is basically the net interest spread or net interest income. It’s the same here. The insurers invest the policyholders’ premiums (lump sum or periodic payments) and that investment portfolio earns a “yield”, which should exceed the cost of those policies (i.e., what the insurer has promised to pay) by some target margin or spread.

For example, if BNRE earns 20% on capital, reinvesting in this business is a good thing. Many investors would likely agree the opportunity cost of equity capital for such a business is probably around 10%, so this business is earning “excess returns on capital.” The higher the excess return you can make, the better, obviously. Furthermore, BNRE can grow and so has the capacity to reinvest at those 20% rates of return. Because it can do this, BNRE is worth more than if it couldn’t grow, and you as the investor would prefer that they retain and reinvest BNRE’s earnings. If it couldn’t grow, there would be no opportunity to reinvest and it would instead distribute its profits to us. We’d then be taking the money and trying to earn our 10% opportunity cost, instead of the 20% BNRE makes on reinvested dollars. So the money is worth more in BNRE’s hands than it is in our hands, and therefore the business is worth more the more it can reinvest. Ideally, you want to be buying into a business where a lot of this future growth and capacity to reinvest isn’t already in the purchase price, so you as the investor are going to capture this value over time. Obviously, this is hard to do, since any informed seller is going to know the business has a lot of future potential to create value, and is going to negotiate for it. That leads us into value investing and having an edge, or some information/perspective/behavioral advantage the other guy doesn’t have, so that you can get such assets for cheap and earn those attractive returns.)

In fact, in my whole career, this is the first time I’ve found a business this good for half of intrinsic value.

picking up what you're putting down