Banks Update (2 / 2): ALLY

And some cheeky bonus stuff

~15 min read

Continuing where we left off…

Ally’s earnings, and the extra twist to this bank’s thesis

The Ally thesis is deep in green light territory. Its loan portfolio is doing exactly what I thought would happen and management is deftly navigating a somewhat difficult environment. I think we have a solid base hit here.

While BAC needs industry deposit growth for us to win, and it’s important at Ally too, you might recall Ally’s main driver is something else entirely.

To review: we are primarily watching Ally’s net interest margins (NIM) expand.

Normally, it is stupid to base a bank investment thesis on its NIM, because you can’t predict interest rates. Much human effort is wasted on this. People will tell you it is not futile. Those people are wrong. They try even though bank CEOs themselves say you cannot predict NIMs.

We are allowed to break this rule at Ally.

This bank is liability-sensitive (its NIM falls when interest rates rise quickly) whereas most banks are asset-sensitive (their NIMs rise when interest rates rise quickly). Ally’s NIM is very likely to expand in the next 2 years, and Ally doesn’t need to do anything.

By now, you guys know that net interest margins are driven by deposit costs and by loan and securities yields. So you know I’m going to outline two interacting reasons Ally’s NIM is likely to expand:

On the liability side of the balance sheet, Ally has a high “deposit beta”. Its deposits are mostly big-ticket online savings accounts people will readily move if the rate isn’t sufficiently competitive. BAC and WFC have a low beta because they have your sticky small-balance-daily-checking-accounts. Ally’s deposits will swiftly and closely follow market rates when the central bank makes moves.

On the asset side, Ally’s most important book by far is the car loan book. These are fixed rate loans. Ally’s book therefore doesn’t reprice when market rates move, even though the going rates — the “spot” rates in the market — for car loans rise/(fall) almost immediately when the central bank starts raising/(cutting) rates. Instead, Ally’s customers have to pay down their loans, then Ally has to make a new one to a new customer at prevailing market rates.

So Ally is very different from most banks. If deposit rates stop rising, which they have now, Ally’s NIM will increase as its loan book still turns over into higher yielding loans.

This is happening. We went over it last quarter, and it’s ongoing.

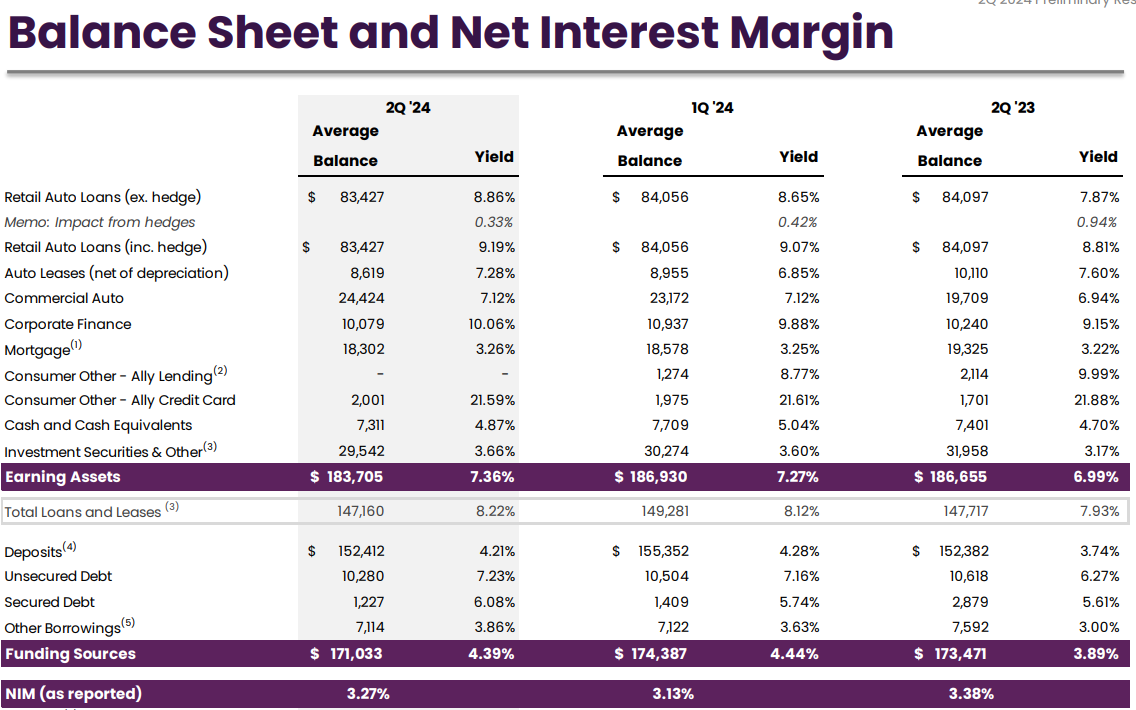

Let’s take it up a notch and show you a big boy table, a bank’s net interest margin table.1 You know enough for me to hit you with this bad boy:

Aaaaaaaaaaaaaaah. Numbers everywhere! Stop complaining, this bank is simple. You should see Bank of America’s!

(Ok, breathe: Think of a bank as a “spread” business. You take money like deposits from one guy, called “funding sources” above. You lend the money to another guy as loans and securities, called “earning assets” above. Then, you pocket the difference, which is the “spread” or the “net interest income/margin”. Meantime, you try not to have too many borrowers default on their loans. This table summarizes that. Funding sources is where the money came from and what it cost, and earning assets is where the money went and the yield it’s getting.)

Since the US Fed has left interest rates alone a while, you can see Ally’s deposit rates have flattened off, at 4.21% vs. 4.28% last quarter, vs. 3.74% when we were around the end of the rate hiking cycle last year. Unless inflation goes to 8% and the Fed needs to go back to war and raise interest rates, we are at the top of the mountain. Ally’s deposit costs will bump around this level. Deposits, and deposit rates, dominate Ally’s funding (liabilities) and thus dominate the cost side of its net interest income spread.

On the asset side, you can see car loans (plus mortgages and investment securities2 dominate Ally’s earning assets. The mortgages are long-term fixed-rate mortgages. The bonds are fixed-rate. And the car loans/leases are 3-6 year fixed-rate. Fixed-rate. Fixed-rate. Fixed-rate.

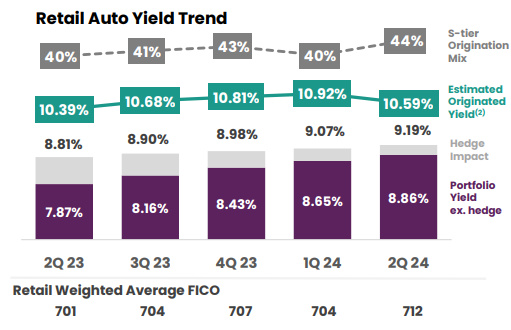

The consumer auto loan book is the biggest guy in terms of raw size, and also earns a higher interest rate, so it disproportionately contributes to the revenue side of changes in the net interest income spread. You can see rates in this loan book are still rising steadily — to 8.86% from 8.65% last quarter and vs. 7.87% last year3 — even though the Fed is done hiking interest rates. So the loan rate is up 0.2ppts and the deposit rate is down 0.07ppts. The NIM wedge is widening.

To keep hammering this home, this is because older loans (the “back book”) are being paid off, and those are from a time when interest rates were lower, like 2020/2021. Current auto loans of the kind Ally likes to make have ~10.5% interest rates in the market today, and Ally is “rolling” the book into these new, higher rate loans (the “front book”):

This is pulling the average rate on the portfolio upward.

This will keep happening for ~1.5 years until the whole portfolio contains loans originated around these rates. Deposits will bump around 4.3% while the big, important loan book’s yield goes from 9% to 10.5%, at which point I make big money and cheer loudly.

But wait, you guys are smart. You are thinking: “Well, rates could go up or down, Chris. If you’ve told us anything, it’s that you told us the only thing you can know about interest rates is they’ll fluctuate.”

Yes. Fair. Very fair. Now here’s the difference between being a mediocre vs. a good investor. You are thinking in probabilities and a range of outcomes.

So let’s get more nuanced. Rates can do three things:

Go up

Stay the same

Go down

If they go up — wherein you’d have to believe we go back to high-inflation-world and the Fed has to keep climbing the mountain (for which there’s little evidence!) — our thesis will be delayed. Central bank beatings would continue until inflation morale improves. Ally’s NIMs would stay under pressure, since its price-sensitive deposit costs will rise faster than the auto loan book reprices and that lag effect won’t unwind until the end of the hiking cycle.

If we go down the mountain instead, our thesis accelerates for the same reason. Deposit costs would fall faster than auto loan portfolio income, and NIMs would quickly rise.

If we stay where we are (the base case), NIMs go up as described.

In two of three scenarios, we win. The bad scenario also has by far the least supporting evidence and appears the least likely.

And so in summary we have the CEO saying this quarter: “We expect to exit 2024 near 3.5% and continue the march to 4% NIM as our lower-yielding back-book continues to be replaced by higher-yielding originations. And as we've said before, our 2024 exit rate is not dependent on Fed rate cuts. We expect a 4% NIM run rate to be reached at the end of 2025 in a range of rate scenarios.”

At the risk of popping the champagne bottle too soon, here is a meme.

| Video clips by quotes | a566bafc | 紗")

See why I picked this stock? You want highly asymmetric bets (“high convexity” in finance). You want limited loss potential to preserve capital, and big-time greed on the upside. And when you are quite sure you have those things, you need to be an adult and rationally recognize you have no choice but to bet hard.

New CEO

Ally’s CEO Jeff Brown left recently.

I thought they’d promote Doug Timmerman, who runs the auto lending business. The board brought in Mike Rhodes instead, who had been running Discover Financial.4 I liked what Brown said during the search process, that they’re looking for a steward of the business, which is how I felt about Brown. Rhodes sounds similar so far. He also brings a wealth of consumer banking knowledge, particularly on the credit card side.

I am looking for Rhodes to focus on a few things and not touch others:

Leave auto lending alone. Timmerman and team are doing a fantastic job navigating a hard environment using the competitive advantages they built. Rhodes clearly said he only wants to polish this diamond.

Grow card and the commercial business. Discover’s bread and butter is a consumer card business. It wasn’t Brown’s. I’m hoping Rhodes can get this thing going because credit card businesses nearly always have fantastic ROEs. Ally has a huge opportunity with 3.2 million depositors and another several million other relationships (e.g., 4 million auto loan borrowers), only a fraction of whom use or are aware of Ally’s no-fee credit card products. (Start marketing!) Card may be a no-brainer for Ally. On the flip-side, Ally has disadvantages (lack of scale necessary to provide good card rewards) that will make it harder to actually acquire the kind of cardholders everyone wants (big spenders who sometimes revolve balances and who barely default on loans). So far, Rhodes thinks other businesses need capital and are earning attractive returns on capital, and wants to push his chips that way. I’m OK with this.

Keep nurturing the nascent commercial lending business: this is a multi-$ trillion industry. Ally is a tiny, tiny piece of the pie. There are plenty of pockets with good risk-adjusted margins where Ally can win. Rhodes has less experience here but Ally already has an established commercial lending team and infrastructure, and the business is earning excellent returns on capital. Rhodes wants to press this bet.

Continue acquiring depositors: Ally has few online bank peers who are as good as it is. Net promoter scores and other measures are very good. There are so many tiny, poorly-managed banks in the US who have little chance of building a strong online-and-in-person distribution footprint. They are collectively losing share to the big guys and to online banks like Ally and Capital One. Rhodes doesn’t want to mess with what’s already working here.

Loan securitization is also something Rhodes seems to want to do more of. I’ll explain these shenanigans at the end.

I like Rhodes’ starting point: “my primary focus is to execute on the plans we have in place … don’t expect any significant near-term shifts.” Most of his comments were framed in terms of capital allocation. He’s clearly thinking “where do I reinvest the next dollar such that it earns the highest risk-adjusted return?”

What he didn’t talk about is cross-sales, which Ally is doing and needs to keep doing to bring down its deposit costs. You can’t expect someone to cover everything all at once. We’ll see.

Some new information and thoughts on risks:

Ally has 1,000 people dedicated to collections, out of 4,500 people in auto lending. 600 of 4,500 are underwriters (who make the loans), with 12 yrs average tenure.

We’ve more people in collections than underwriting. I have heard other banks mention underwriters and underwriting capabilities many times, but I’ve never heard one mention collections. I know in the case of credit card for example that collections are often outsourced5.

This weakly supports the idea others can’t compete in Ally’s market segments because they don’t have the collections capability (which I talked about in the original thesis). Other banks generally are originating loans to much higher quality credits (people with stronger financial situations and histories), who tend to default a lot less, meaning you don’t need to invest in collections and work-outs. To compete with Ally, other banks would need to structurally increase their cost base, which is especially unpalpable in the current high-wage-inflation environment.

The evidence would be stronger if I knew more about the collections labor mix at other big auto lenders like Wells Fargo.

Death by deposits: Ally and other banks are dealing with deposit outflows. If Ally can’t continue to onboard new depositors at a good clip in the current environment, its depositor base will start shrinking and it will deleverage a bit on its fixed costs, at least until industry deposits start growing again. New customer growth is generally masking the fact that per customer deposits are declining because there are better rates to be found in money markets and such, and Ally is basically pricing deposits such that its deposit growth matches funding needs instead of maximizing deposit growth. The declining per customer deposits are an industry-wide problem, which we’ve touched on a few times.

To Summarize

Our NIM thesis is clearly working. With the stock moving from high-$20s to >$40 and outperforming the market, the market looks like it’s coming to see our thesis.

What hurts our thesis? If you think…

interest rates are going to 8%, in which case there’s going to be a lot of pressure on Ally’s NIM and a lot of pain in its securities book, or

We are going to have a depression where loan losses are so bad it overcomes Ally’s PPNR (which can sustain a very high ~4% annual loss rate, more than double what Ally’s underwriting to and where it’s historical underwriting record reflects skill and discipline), then…

… then the investment’s not going to work out so great.

Although the stock’s ripped, I’m not thinking “sell”. Things have only half played out.

$5-6/share in ~2026 earning power at a 15%+ ROE6 certainly isn’t fully priced in at $42/share. Future balance sheet growth isn’t priced in either. That’s despite the fact Ally’s taking market share at a good clip, adding ~6-10% more depositors annually, and has <1% of America’s deposits. It has many opportunities to put those deposits to work in growing businesses like the commercial loan book (which is earning over 20% on capital) and I’m still excited to see what Ally looks like in a few years. The stocks worth $65-80 if the evidence continues to support our thesis.

Funny Business

Let’s end with a bit about how banks do cheeky things to circumvent regulators, how they have to do this, and why it’s cheeky-but-not-malicious when done in moderation.

OK, before starting this part, know that there are essentially no angels in the financial sector. Even Berkshire Hathaway has done questionable things; I still think management are very honest. I think Ally’s management is prudent and honest.

This said, here’s how cheeky things begin.

Warren Buffett owned Freddie Mac in the 90s, and eventually sold it, recognizing the company was at the epicenter of the growing level of funny business going on in the US housing market, which eventually blew up in 2007/08. Ally is now doing some things that rhyme with those things. Understand though, there’s an appropriate level of “capital management” all banks do all the time, and then there’s an inappropriate level of funny business some banks and other financial institutions sometimes do.

Ohhhhhhhhkay. What’s this slide say? It says “regulatory arbitrage” and “financial engineering” but using words like “Capital Optimization”, which don’t raise eyebrows.

It says the regulator says if Ally has $3 billion of prime auto loans, those loans carry a 100% risk weight. Although not on this slide, regulators also say Ally must hold 7.1% common equity tier 1 capital (CET1) against its risk-weighted assets. It must retain an equity capital buffer on its balance sheet, of 7.1% of those loans.

For these auto loans, Ally must retain $3,000 million * 100% risk weight * 7.1% CET1 = $213 million.

But, Ally’s allowed to divide that same pool of loans up into tranches (slices), which are different legal entities that can be kept or sold.

The different tranches are arranged in a cascading “waterfall”. Say the first tranche is $300 million out of $3 billion. Say $30 million of borrowers default and loans are lost. The whole structure does not share the $30 million loss. Instead, that lowest $300 million tranche takes up to $300 million of losses first, so it eats this whole $30 million loss and sees a 10% default rate, while all the other tranches lose 0%, even though the overall loss rate on this $3 billion loan portfolio was $30 million or 1%.

If the losses then go above $300 million, the second tranche eats those losses, and so on all the way up to the safest tranche at the end. In simplistic terms, this means the first tranche is the most risky and the last is the least risky.

Since the risk levels are different, the amount of capital the bank needs to hold against each type of tranche is different. The riskiest ones should carry a higher risk weight and the less risky ones should carry a lower risk weight. Although this is not the best logic, the regulator says this is the logic to use.

Back to the slide now. The sneaky thing Ally’s doing is tranching up this $3 billion pool of car loans into 3 pieces and selling the middle one to another guy. It keeps the lowest and highest. It is probably keeping the lowest because that creates an alignment of interests between them and the guy buying the middle tranche (who thinks “well Ally is going to lose money before I do, and Ally is the one making the loans, so they have an incentive to make high-quality loans”). It is then keeping the best tranche for itself because that one is now “safer” and has a lower risk weight.

By getting rid of a piece in the middle, the small piece at the bottom gets a higher risk weight, but the really big piece at the top gets a lower one. When you do the weighted average of those, it turns out this brings down the aggregate risk weight. This means Ally no longer needs to hold proportionately as much capital on its balance sheet. Rather than holding $213 million against $3 billion of loans, Ally will hold $2,600 million * 20% RWA * 7.1% CET1 + $45 * 1250% RWA * 7.1% CET1 = $36.9 + 39.9 = ~$76.8 million, against $2,600 + 45 = $2,645 million in loans, or only 2.9% in common equity capital, instead of 7.1%.

Said another way, they save ~$213 - 77 = $136 million in equity capital on the balance sheet. They hold 64% less capital, but are earning almost the same net revenue as they’ve held onto 88% of the loans ($2.645 billion of 3 billion). Ally reduced its capital intensity by more than half.

Cheeky.

What’s really going on here is that Ally’s management knows — and I already thought a lot about this and agree — the bank has more capital and earning power than it needs to survive a severe storm at sea. So they’re doing things that can reduce how much capital it’s holding, but within the bounds allowed by regulators. The less capital they hold to run the business, the higher the returns on capital.

Every bank does some of this. Otherwise 30 year fixed mortgages wouldn’t exist. What’s not OK is if you take it so far that you introduce big underlying risks at the bank or even systemic risk and misaligned incentives across the system overall, and you create an epic boom-bust cycle like the US housing crisis.

The real takeaway though is that banking regulators should come up with smarter frameworks for the industry to exist within by taking account of the fact that banks and other players have agency and will take actions in response to regulatory change. We don’t live in that world, sadly. We live in this silly one.

Enjoy your weekend!

Chris

All American banks provide a net interest margin table.

This is very high-grade stuff like 30-year fixed-rate US Treasury bonds.

Excluding Ally’s hedging activities, where it’s using pay-fixed-receive-floating interest rate swaps, a kind of derivative contract, most likely with a group of other banks. Don’t get me started.

It’s merging with Capital One and no way is Rich Fairbank stepping down; Capital one is one of our “small bets” in the portfolio, by the way. It ripped like 50% as I started working on it and bought a little, and now it’s just a tiny position I continue to learn about. *Shrug*

See the annual reports of PRAA, or PRA Group, a collection company.

Although too hard to derive quickly for you, I’ll mention that incremental loan economics are in the 15-25% ROE range.