Portfolio Intro

Where we sit today

First, happy weekend! I hope you enjoy this Saturday morning read as much as I enjoyed the write. I’ve received a bunch of feedback and encouragement already, and so thank you very much for your support.

Safe harbor statement and huge disclaimer: There are stocks below. May God and securities regulators bear witness, I am not your fiduciary or financial advisor! Please don’t go and buy this stuff without doing your homework. I may or may not own all these in a month; maybe I changed my mind about an idea, maybe we found something better than what we own.

Not to mention, stock market investing is like chainsaw juggling: It’s completely safe if you catch them by the handles, but that takes serious practice if you don’t want your digits hacked off during a live performance. If you want to start with sharp stuff rather than oranges and bowling pins, there are other places for that. Like r/WallStreetBets. Don’t do that here. Keep your hands intact.

Before we dig into companies, industries, investing insights, etc., I wanted to start with an intro to (1) what we own and a portfolio-level view, (2) the recent actions we took to get here and a little brief on those investments, and (3) a bit on our concentrated investing & portfolio management style.

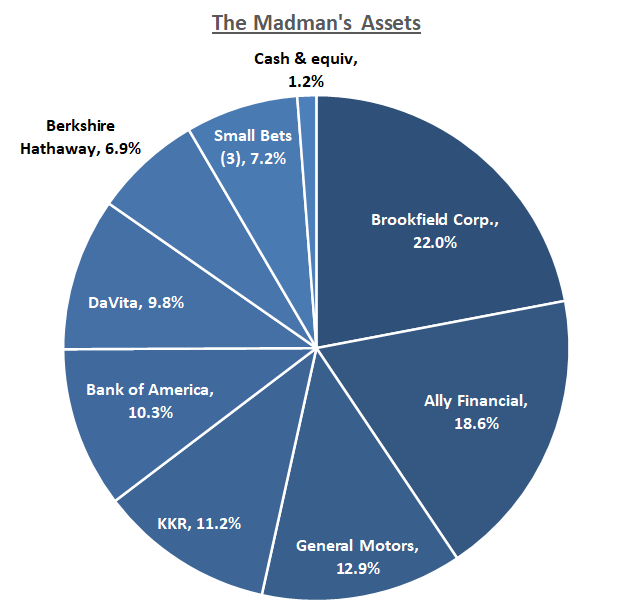

My portfolio’s below. This is our (meagre) net worth, meaning we treat this money like it’s holy. I also run someone else’s portfolio, which looks similar except for a larger Berkshire position. Those dollars, too, are blessed and revered.

We like our positions at today’s prices. More than we usually do. Even though many are cyclical, we like them through a recession. Hence, we’ve been fully invested.

It hasn’t always been this way, but our current portfolio is likely to be volatile, highly correlated to “market sentiment”, and levered to the state of the US economy. This is because of two things.

First, we own mostly cyclical businesses. When the market takes a “risk-on” or “risk-off” attitude, our positions can move a lot more than, say, stable businesses like Procter & Gamble, Diageo, or Wal-Mart. After Fed Chair Jerome Powell’s Wednesday speech, Brookfield fell >5% in 2 days on what appears to be increasing fear that higher rates will stunt its growth in client relationships and harm certain of its investment funds’ near-term performance.

Many of our businesses’ near-term profits, like GM, BofA, and Ally, will depend on how the economy is doing at the time. They’ll make less in a recession. Though they can’t be predicted, recessions are inevitable and the consensus view (which may well be right because there’s plenty of supporting data) is we have one coming. We’re rafting calmly on the river today, but the current of time pulls us inexorably downstream to where there’ll be white water rapids at some point.

Second, we currently only own what Buffett in the 1960s called “generals”: generally undervalued and under-appreciated businesses yet where there’s no obvious short-term catalyst to realize value. They often have some kind of problem, where our bet is that problem’s temporary. It’s not the 1960’s though, and the US market — now full of thousands of amateur stock pickers and hundreds professional active fund managers — tends to show a lot of price momentum against changes (up or down) in performance metrics that drive a company’s near-term growth and returns on capital. It’s a deep and efficient market that often prices things in quickly, especially for larger companies. If for example KKR and Brookfield started raising a ton of new client money and generated huge investment gains compared to recently, the stock’s tended to follow as the market notices. The opposite’s also true.

Because of the current portfolio composition, if there is a serious recession and the market falls a lot, we should be highly correlated and will almost certainly take it in the chin quite hard. We’re also likely to out/underperform if a few cyclical sectors like financials fall into/out of favor in a big way. That’s just how things will be. You can argue it isn’t ideal, and that’s because it isn’t ideal, but if you can find me The Assets That Only Go Up A Lot Regardless Of The Future, Never Go Down, And Don’t Already Trade at 30x Earnings In The Current Market Environment Simply Because They’re Not Cyclical, you call me right away. I’m actively looking to find less cyclical stuff that still has compelling risk/reward, but I think that’s going to need to happen outside the universe of large US businesses. I’m thinking of moving over to Interactive Brokers (no affiliation) to make international investing easier and cheaper. If I could find something as compelling as I find Brookfield and that also wasn’t cyclical, there are certainly things in the portfolio I would sell for it.

Nonetheless, I think we own multiple 50-cent dollars that have smart managements and range from decent-to-incredible quality businesses. I think there’s levers many can pull to protect their profits in a recession and continue to grow their underlying value.

We’re focused on value vs. price, not where the prices will go in a sell-off, and we did our buying at prices we think already reflect a recession-driven slowdown in these companies’ profits. As we said earlier this week, if you reverse-engineer GM’s price for example, expectations for low car sales and no near-term profits are already implied.1 Will the stock still sell off if the market falls 30%? I’d be shocked if it didn’t. Will a recession permanently impair our investment? No, because of the price we paid and those embedded expectations. And that’s how we’ve tried to embed long-term downside protection the portfolio’s value.

Looking out 5 years, we like where these businesses are going. As a group, we think:

Because the market’s missing something, we bought them very cheap relative to their potential and think there’s little downside if we’re wrong,

We know these businesses well,

They can generally reinvest at much more than the opportunity cost of capital.2

They’re run by prudent, shareholder-friendly, and skilled CEOs and business builders who have track records of managing well for years, and

They all have the balance sheet strength to survive even a severe economic storm.

Through the economic cycle, our ideas’ success should mostly depend on: (a) management execution, (b) certain multi-year industry tailwinds we expect, and (c) no huge tectonic shifts in the companies’ industry structures.

The last thing about the portfolio is the most obvious: it’s clearly very concentrated.

Historically, we’ve always been this way. The top 5 investments usually made up >60% of our capital. We’ve typically owned 8-15 at a time. Today, it’s more concentrated than usual: >90% of the portfolio is in 7 positions, of which 3 make up >50%.

You might also notice Ally / Bank of America, and KKR / Brookfield are competitors in two industries, so we’re concentrated by industry. Five of our seven large positions are financials, although they have 3 completely different business models and are often “internally diversified” as you’ll see. Six years ago I thought I would never understand most financial companies well enough to invest. Now financials are the bulk of what we own. We learn.

Some may wonder how we sleep at night without tossing and turning that our largest position could drop 30% next year. Well, we sleep in a bed, like everyone else.

First, this is not my first rodeo. I’ve watched my top position fall 55% only to >3x a year later. While I already had a good stomach to begin with, trial by fire can build resilience. Equity investors can instead own an index fund and watch a diversified stock portfolio fall just as much since the average stock correlation is very high, and is highest in a general market sell-off when people flee to the safety of cash and bonds.

Second, I mean: if you look at plenty of people’s balance sheets, most of their net worth is in one asset, their house. It can’t be rented for profit because they live there, and everything other than the land its on requires capital reinvestment to maintain its value. And most of that value is capitalized by mortgage debt, whereas our personal balance sheet is about 95% equity, 5% debt. We look diversified, cash-generative, and well-capitalized by contrast. We also have a tighter confidence interval around the value of our businesses than most can likely have about the value of their home in 5 or 10 years.

That’s the high-level view of our portfolio’s characteristics and the companies as a group. We’ll put some more numbers around this in the near future.

Note the portfolio has overlap with Berkshire’s portfolio. There’s influence, but it’s not typically intentional. These positions came through my own idea generation and screening, and my work is my own.3

Activity:

I hadn’t done much since 2020 (partly because I was busy with personal and professional things vs. generating new ideas), but in 2023 I returned to the game in full force. I found several ideas I liked more than what I owned and we’ve turned over nearly half the portfolio year-to-date.

That’s a lot of churn, but our hold period for ideas that are working is usually long: I’ve owned Bank of America since 2020, KKR since 2019, DaVita and General Motors since 2018, and Berkshire since 2010. Owning them through recession and company-specific problems has added depth to how I think about them and about long-term investing. I think it’s made me more level-headed and sanguine.

This year we bought Ally and Brookfield in Q2 and Q3, respectively. They’re our top positions. We didn’t do that on a whim: we’ve followed both (and their industries) since at least 2018. We often go after things that other people seem to not like at the time, so it’s no surprise we bought Ally during this US regional banking crisis and Brookfield when higher interest rates and office real estate vacancies are (and will continue to, at least for a while) pressure parts of its business.

For now, we’ll talk briefly about each and what we’d sold for them.

Because the we’ve been fully invested since 2019, we sold positions in Wells Fargo (~10% weight; bought in 2018, 2020) and JPMorgan Chase (~5%; 2020) to source funds for our Ally purchase. All three are US banks.

The reason’s pretty simple: I find Ally more compelling, so we switched. Although we don’t think we can foresee Ally’s future with as much confidence as Wells or JPMorgan and so there’s a little more uncertainty, we think the risk/reward is far better. Don’t conflate uncertainty with risk, by the way. They’re not the same.

Both Wells and JPMorgan are still undervalued, in my opinion.4 Even though I sold at a small loss, I don’t think Wells is a total mistake, but it’s taking much longer to fix the business than the 5 years I originally underwrote in 2018 after speaking with contacts in back-office banking. JPMorgan was a winner. It’s a fantastic bank taking market share from an already-leading position. There was nothing wrong with it other than the fact the world was going to end in 2020. Most bank stocks ripped when that didn’t happen and government bailed out consumers and small businesses.

By the way, if you don’t read JPMorgan CEO Jamie Dimon’s annual letters or listen to his interviews, you should start. They don’t make a lot of people like this guy.5 You’ll wish you had him running every company you invested in.

I bought Bank of America in 20206 at the same time as JPMorgan and for the same reasons but haven’t sold because the risk/reward is still attractive vs. where we think the bank’s going. Also, like “overdriving” your high-beams at night, I think we’d be over-betting our knowledge and confidence with a 30% Ally position. We’ll talk about Bank of America another time, but suffice it to say that (1) with respect to its unrealized losses in its securities holdings, we think many are concerned about a non-issue and aren’t looking at the balance sheet holistically (which, if you ask industry insiders, is how all good banks are managed internally), (2) the upcoming credit loss cycle for the banks will very likely be more benign than 2009, and (3) the industry will return to mid-single-digit deposit and loan growth soon enough, while BofA continues to slowly grab market share.

To make room for Brookfield, I reduced some positions and sold other small ones (including two mistakes). That’s how the portfolio got so concentrated.

Unless it turns out I am wrong or the stock looks clearly overvalued, we intend to hold Brookfield for a very long time. This is an incredible business that will take more than a decade to exhaust its market opportunity. Brookfield Asset Management (BAM), its largest business, may triple in size between now and then. With nearly 60% margins and no need to invest capital to grow, BAM’s economics make even Google’s ad business look like a joke.

Ally Financial (“Ally”; ALLY):

Ally’s America’s largest online bank.7 It originally grew out of GM’s in-house auto financing business, General Motors Acceptance Corporation (GMAC), and was split off in GM’s 2009 bankruptcy. Since GM would eventually regrow its financing arm, Ally built relationships with other automakers and their dealers. It also went into used vehicle lending, a market 3-4x the size of the new vehicle market. It’s now one of the largest used car lenders in America. At the same time, it built an online bank and replaced its wholesale debt with lower cost consumer deposits to fund its auto loans. Going forward, Ally’s in the process of stitching together a diversified consumer and commercial bank with credit card products, a retail brokerage business, and commercial lending.

We paid in the high $20s for Ally and think if we’re right it’ll be worth $53-76 in ~5 years (2-3x our cost; plus a >4% dividend). There’s line of sight to a 2x even through a bad recession, although there will be some pain and gnashing of teeth if that happened. We paid ~0.85x tangible book value and ~5x net profits for a business we think can do teens returns on equity and earn $5.50 per share in a couple years. It will retain and reinvest a good chunk of earnings at those returns because it’s taking market share at a good clip, growing deposit customers 10% per year historically. With only 0.8% of the industry’s deposits, it has a huge runway ahead. Banking in the US is fragmented and many small banks are in deteriorating competitive positions with no moats to defend their economic castles. As a group, they’re slowly ceding market share to online players like Ally and to well-run deposit-gathering behemoths like JPMorgan and Bank of America. That’s going to continue, although we don’t even need it to happen for the investment to win.

We traded uncertainty over Wells Fargo’s asset cap for concentration in Ally’s loan book, which skews heavily to used and new car loans. From our research, we concluded they’re shrewd vehicle lenders, even more so than Wells (long regarded as one of America’s most conservative lenders). The loan book will be more diversified in the future because of what management is building, but even today we could ride this concentrated book through a recession. Although there would be elevated credit losses, we believe we’ll emerge more or less fine. That’s partly because of (1) the company’s lending discipline and superior analytical capabilities vs. competitors, and partly (2) the strong balance sheets and incomes US consumers have today. It’s a good time to make an 11% used car loan to people who still have a lot of excess cash from COVID payments in their checking accounts and who are unlikely to remain unemployed long because the labor market’s still tight.8

Because Ally’s trying a few things at once and running with what’s working, what it’ll look like in 5 years is less clear to me than other positions we own or follow. Yet, the management consistently makes smart forward-thinking decisions that look like things I would do if I were in their shoes and my goal was to build a diversified consumer bank with stickier (read: higher profit margin) deposits than today. Even if these initiatives don’t work, the stock’s priced with such low expectations that we’d do alright with only the existing business.

We’ll do a deep dive on Ally soon enough.

Brookfield Corporation (“Brookfield”; BN):

Brookfield’s a complex holding company that owns many different assets (whole or in part). By complex, I mean I spent many days doing nothing but reading the filings of various entities, understanding what they own and how they’re reporting (because it’s not consistent — even metrics with the same acronyms are calculated differently at different subsidiaries) and then combining all that stuff together after making several judgements about their likely cash flows. If you don’t like fishing for ideas then sitting around with a magnifying glass playing “investment detective”, this stuff’s not fun. You could try and make it fun by skipping the reading-and-thinking part to do the buying-and-selling part — which a lot of money managers do — but that works about as well as training for a bodybuilding competition by only eating delicious proteins while dodging the hours in the gym lifting weights.

In any case, BN’s largest asset is a 75% interest in Brookfield Asset Management (BAM), an alternative asset manager. It invests >$400 billion of institutional and high-net-worth clients’ money into infrastructure assets, real estate, and private equity & credit. I estimate BAM’s just over half BN’s intrinsic value. The rest is a collection of many durable assets like high-end offices and city-center luxury retail malls, hydro dams, pipelines, railroads, ports, an annuity insurance business, etc, often owned alongside clients and other investors. Many of these assets’ revenue and profits are derived from long-term contracts where rates escalate with inflation. The cash flows from all these businesses find their way to BN as dividends and asset sales, which management then promptly reinvests into new deals on our behalf.

We bought Brookfield at $33-35. We think it’s worth over $60 today, and could double that value in 5 years. That might also make it clearer why we’re not concerned with the large 20% position: even if BAM were worthless, we’d have paid at worst a fair price for all the other stuff BN owns, and we certainly don’t think things like hydro dams, ports, shipping container leasing, and nuclear reactor maintenance are going to disappear as businesses or even change much any time soon. BAM’s business itself is diversified across many kinds of investment funds as well. As interest rates and inflation rise for example, private credit and infrastructure funds become more appealing to clients and also earn more, while core real estate and private equity assets may struggle more for a time. So our portfolio’s more diversified than it seems, and BN has a lot of downside protection. The same is true of KKR, where the asset management business is about half its value (and is also diversified across various funds for clients) and the other half is a collection of balance sheet investments, such as alongside clients just like Brookfield. Between these and Ally, maybe you noticed a trend of looking for downside protection and of us trying to win by not losing.

BN’s priced around 12x free cash flow even after assuming (a) higher interest payments on the debts against its many underlying assets, given prevailing interest rates9, and (b) several pieces of office real estate are worthless given high vacancies the biblical office exodus that work-from-home caused in many cities.

All-in, Brookfield earns about 17% on equity and retains nearly all its free cash flow to reinvest at teens rates of return. It’s currently investing the bulk into building an annuity/insurance business it believes it can earn 20% returns on; that playbook’s already been run by others and is also really-low-hanging-fruit kind of stuff, so our view’s odds are good they’re adding big chunks of intrinsic value for us. The management are excellent capital allocators and have a demonstrated, decades-long record of earning attractive returns. They’ve also built several Brookfield businesses from nothing into industry leaders. It has scale yet is still a tiny player in huge markets: Brookfield and its clients own something around 0.1% of the world’s infrastructure assets by my estimate, for example. Even with competitors around, there’s plenty of runway for Brookfield to use its sourcing capability and execute on deals to invest our cash flows.

Hopefully that starts painting a picture of why we’re excited to be owners in this business, and why we own a lot. We’ll go over Brookfield in depth later on.

I have mostly the same thesis on KKR and BN.

A few more words on our concentrated style:

It’s a lot to explain all at once how we think and to go through the potential downside in each position. What we said about Brookfield’s inherently diversified business might have helped you get a sense: (1) its asset management revenues are incredibly sticky and are not going into decline any time soon, and (2) the assets in its portfolio generally constitute the backbone of the economy, won’t be made obsolete, often have long-term contractual revenues with inflation protection, are diversified across several sectors, and make up most of the stock price today. We also talked about how Ally has low risk of loss because its loan book is well-managed, it’s consumer borrowers are in great shape, and none of its business plans are already priced in.

Consider a few other things.

Business durability: Our large positions are in businesses we think have durable models where (a) the demand for their products comes from fundamental consumer and business needs that are very unlikely to be rendered obsolete, and (b) the industry structure or market segments they operate in are relatively entrenched and reasonably attractive, so the competitive position is decent and unlikely to change any time soon.

Position sizing and downside: second, we do a “pre-mortem” on each. We ask how things could go badly wrong for the business, and what the value of its cash flows look like in that world. Those values are our downside. We then size positions such that we think we’d be quite unlikely to lose over 5% the portfolio. Thus, even if we make several mistakes, we are never kicked out of the game and always live to fight another day.

Again, if we make it hard to lose, the only other possibility is: we will eventually win.

This has worked. As I go back through the portfolio in the last decade, we haven’t really lost more than 5% of the portfolio on any investment vs. our cost. Some realized losses were even sold at a time where we used the money to buy something else in the middle of a broad market sell-off, so the “holes” in the portfolio were quickly filled when the overall market recovered. Sometimes, we’ve sold losers at a gain because we got them so cheap. Others, like DaVita, have performed below our base case but the margin of safety was so huge that it’s still earning an excellent return for us. We’ve avoided big losses despite the fact we regularly take 10-20% positions (even a 40% position once before). I’d like to believe that if I have any skill at all, it’s been in avoiding being hit by torpedoes. This isn’t to say our stocks’ prices don’t go up and down a lot, because obviously they do. What we’re saying is we’ve been decent at avoiding large, permanent losses of capital in businesses that simply don’t recover.

Hopefully that was entertaining and insightful start! Next I plan to touch on the other positions, sprinkled with blurbs on investing. Then we’ll get into a lot more depth.

From you: I’m curious of your feedback on two things. First, what would you like me to change so far, if anything? Second, I’m thinking of a schedule, like a short post on Wednesday’s around 6-7pm ET, then something longer and more detailed on Saturday mornings when you might be fresh, interested, and have more spare time. I mean, obviously you can read this stuff whenever and wherever you want, but… well… let me know.

I hope you have a great weekend!

Chris

Or significant value destruction from the EV investments they need to make to re-tool plants and the supply chain. Frankly, of all our investments, I think GM is the most at risk of having been a mistake.

This means for example that if you think these companies have a 10% opportunity cost, then you think they’re able to reinvest at much higher than 10% rates of return. The exception to this is GM, whose large investments are at a higher risk of destroying value than the rest of what we own.

DaVita, another Berkshire holding since 2011, came through a free cash flow yield screen in 2018. I don’t have a magic red phone to Ted Weschler’s office, so all my insights are my own. General Motors I followed since 2013 and bought in 2018; I don’t really know if it’s Todd or Ted that owns it. I’ve known about Ally long before Berkshire bought it, and had been researching the company prior to Berkshire’s 13F filing. So I swear, I do actually do my own work!

Wells for example is a $150 billion business printing $20 billion annually in spite of the asset cap, and because of the asset cap has nothing to do but buy back shares and pay dividends with the money. The stock trades where it does because the market hates that it isn’t allowed to grow, and few have any insight into when exactly that will change. We paid $47 and then $20something for Wells and thought it would be worth ~$70 in a few years. JPMorgan is one of the best managed and best positioned banks in the world and is likely to hit its targets earning 17% on equity while growing at over 6% annually, for which you’d reasonably pay more than twice tangible book value compared to the 1.95x it trades at today and the 1.35x we paid.

He’s incredibly hard-working, honest and authentic, holds himself accountable, is thoughtful and succinct, and his mind is unreal. He’ll get asked a question in an interview or a conference call, and will immediately and confidently describe why that thing would work or why it wouldn’t work, and what scenarios you need to think about and hedge against, such as to protect the bank, or how you could make that thing better for the bank’s clients or harder for other banks to copy. I think he’s got this gigantic intuitive framework in his head that essentially covers the entirety of how a bank works and competes, as well as the entire plumbing of the financial system.

We bought around the low $20s in Q1/Q2 2020, and added some at $41 in March 2022.

It’s the second largest if you count Capital One, which is growing its branch presence.

We’ll get to show more data on this in the future.

For example, the commercial mortgages against its office properties are floating rate and so the interest payments move up and down. When rates rise, it eats into our cash flows and also stresses those assets’ financial position.

nice article ... with you on Brookfield!