CSU - Bought more

+ Port Changes

~18 min read

Hi team,

Since the Constellation Software report, I’ve increased our position from 3% of the portfolio to 8%, and I was buying up to CAD 3,100 per share. I’ll explain why shortly.

First, let me summarize all the recent portfolio changes.

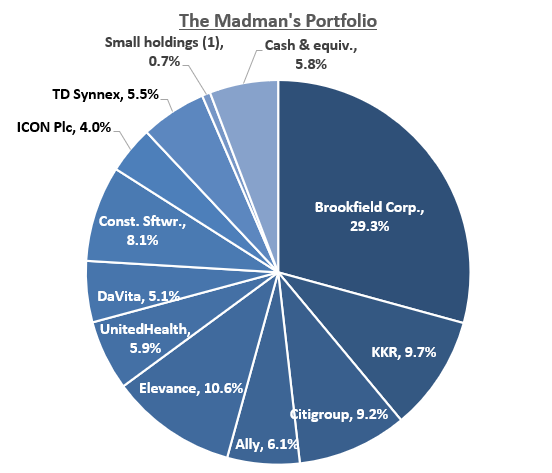

Portfolio

This is the portfolio currently:

Changes:

Citi: reduced 20%. The turnaround is is ~70% played out. The industry backdrop’s favorable, too. At $145, the stock increasingly reflects this. That’s 1.45x ~$100 tangible book value per share. If they can get to the target ~15% ROE and maintain ~5%/yr growth, it’s perhaps worth 2x tangible book value or $200 per share. That’s vs. the ~mid-$60s we paid (~0.75x $86 tangible book value per share) in 2023. A solid “base hit” investment so far, but with worse risk/reward now.

UnitedHealth: reduced ~33%. The ELV+UNH bet grew to >20% of the portfolio, which doesn’t match my conviction level. I kept ELV and sold some UNH. I believe UNH has a tail risk nobody else has. They are more aggressive at trying to capture value by diagnosing MA & Medicaid patients with anything their doctors can find, so that they get reimbursed more from CMS. Other vertically-integrated insurers don’t pull this lever nearly as hard. UNH is capturing excess profit here. However, CMS is trying to curtail this behavior in upcoming reimbursement models. This takes years to happen, and UNH knows it’s coming, so they have time to adapt, but it’s still a bit of a headwind, at a time when I felt we might be over-betting on UNH+ELV.

DaVita: sold nearly 50%. In the last few months, the stock nearly doubled on improved volumes and volume guidance. It trades closer to intrinsic value today. There is still room for it to achieve its profit growth targets, where it’d be worth more like 15-18x earnings, not the 12x it’s at today, but the risk/reward’s worse.

KKR: added nearly 25%, using funds from the Citi & DaVita sales. For years the industry leaders and industry have been playing out exactly as we thought, but KKR is recently plagued with bad news around private credit client redemptions & potential software investment write-downs. Neither of these will harm KKR’s industry position, nor the industry tailwinds. We added at 13-14x its current ~$7/share earning power. We think it’s worth >20x earnings. It continues to earn attractive returns on capital while doing >10% organic growth in the core business, while it’s Global Atlantic subsidiary should see higher future returns on capital as well, as KKR pivots GA’s portfolio toward private markets and optimizes its mix of annuity liabilities. The stock’s worth 1.5-2x the current price today, and can be a 2x from here next 5 yrs. That’s better than Citi or DaVita.

Constellation Software (CSU): increased from 3% of the portfolio to 8%. I’ve kept researching and am gaining conviction we have our arms around the risks & opportunities, and broadly how software/AI competition is panning out. You’ll see below. If CSU navigates the environment well — which we said we think they have the time and capability to do — I think CSU can be worth USD 8,000/share in 5 years, 3.5x the current price. Even if AI start-ups kill more of its businesses than we think, we can still make a lot of money from the current price.

We’re sourcing capital from inferior risk/reward holdings, and tilting that capital toward ideas with better risk/reward.

Other portfolio things in footnote.1

Why More CSU?

I’ve increased the bet because the evidence I’m finding broadly matches the risks/opportunities we hypothesized.

Hopefully I give a decent explanation below…

Meet Lassie

Recently, I saw investment venture capital firm Andreesen Horowitz (now “a16z”) made. It was in a start-up called Lassie.ai. It’s AI for dentist/other clinics.

Oh no, vertical market software (VMS) businesses like practice management systems (PMS) at dentist and doctor clinics are under attack!! Are CSU’s VMS doomed?!

Check out Lassie’s site. The main workflows they’re going after — for now — are “revenue cycle management.” When an American goes to the dentist, you don’t just pay cash/card. There are insurance claims and other things an administrative person has to submit to / retrieve from the insurer, and then enter into and reconcile with the practice’s PMS, which has all the invoice data, etc. For example they have to check the insurance plan deductible or co-pay or any health spending account, so they know how much the person has to pay out-of-pocket vs. what the insurer will reimburse the dentist. For a healthcare provider, billing is complicated. Lassie is automating this. A trained AI agent will head to the insurer’s portal, submit/retrieve what’s needed, update the clinic’s PMS as needed, reconcile things, monitor if the insurer accepts and pays claims or denies them, etc. The dentist can ask verbally on an iPhone app or whatever “what’s the status of our billing today”, etc., and get summaries/analytics, look at any claim denials that need to be resubmitted or justified, etc.

I asked Google Gemini (I like trying all the AI models) to find similar such start-ups. Turns out, there are many. Even just in dentistry. I had Gemini look into each’s product/service info, summarize what they do in a table, then compare this to what a PMS already does.

Interestingly, only one of the nearly 10 Gemini found is trying to re-build the whole software stack and the system of record (the clinic’s database), which are the workflows and the tech stack layers a traditional PMS VMS occupies. That’s the part Constellation Software does.

Instead, most of these start-ups are basically building a skin over the PMS. The AI agent is just a cheaper, faster, administrative employee, connected to the PMS. It goes on insurer portals, grabbing, submitting, and reconciling billing and other data, but still working by using the PMS and managing its data.

Obviously, this is a smarter and faster way to grow your start-up, right? Instead of trying to attack and replace everything, sell a skin that helps automate some of the admin workers’ workflows. That takes only a couple days for the customer to set up and learn, and it interfaces with your existing software & data solution. That’s way easier to sell than if Lassie’s salesperson has to convince a dentist to rip out and replace their entire PMS, a months-long, highly disruptive project, since the PMS literally runs all your daily workflows.

Whether this workflow is integrated into the PMS or not, it also shows there’s new economic value up for grabs:

The dentist is still paying ~$1,000/month (or whatever) for the PMS. Now,

They also pay $500/month (or so) for Lassie AI. So,

The dentist is willing to pay this new $500/mo because it replaces some of the work Susan is doing at the dentist office front desk. Susan costs $4,000/mo, so replacing half of what Susan does saves $2,000/mo, for which Lassie charges only $500/mo. The dentist keeps or reinvests $1,500/mo in economic value saved.

They now need fewer Susans, or, can handle more patients with the same number of Susans. The chain can take the $1,500, hire another dental hygienist for more cleanings, spend it on marketing, let it drop to profit, etc. If Lassie and others do their jobs well, it’s no wonder many healthcare providers are signing on.

Yet clearly, these entrepreneurs aren’t going toe-to-toe against CSU. They’re taking the path of least resistance: building a skin over the PMS, then chasing a different slice of the economic pie, rather than attacking CSU’s slice.

It’s not like I predicted this, but now that I see it, it’s clearly smarter from a growth standpoint. The sales cycle is shorter, i.e., they can onboard new dentists faster, and it probably costs less. But the world is also showing us that disrupting the VMS is hard. CSU is less at risk of obsolescence from new AI-native competitors.

Second, ask yourself “sure, but then what?” Here’s where it gets interesting….

Land and Expand

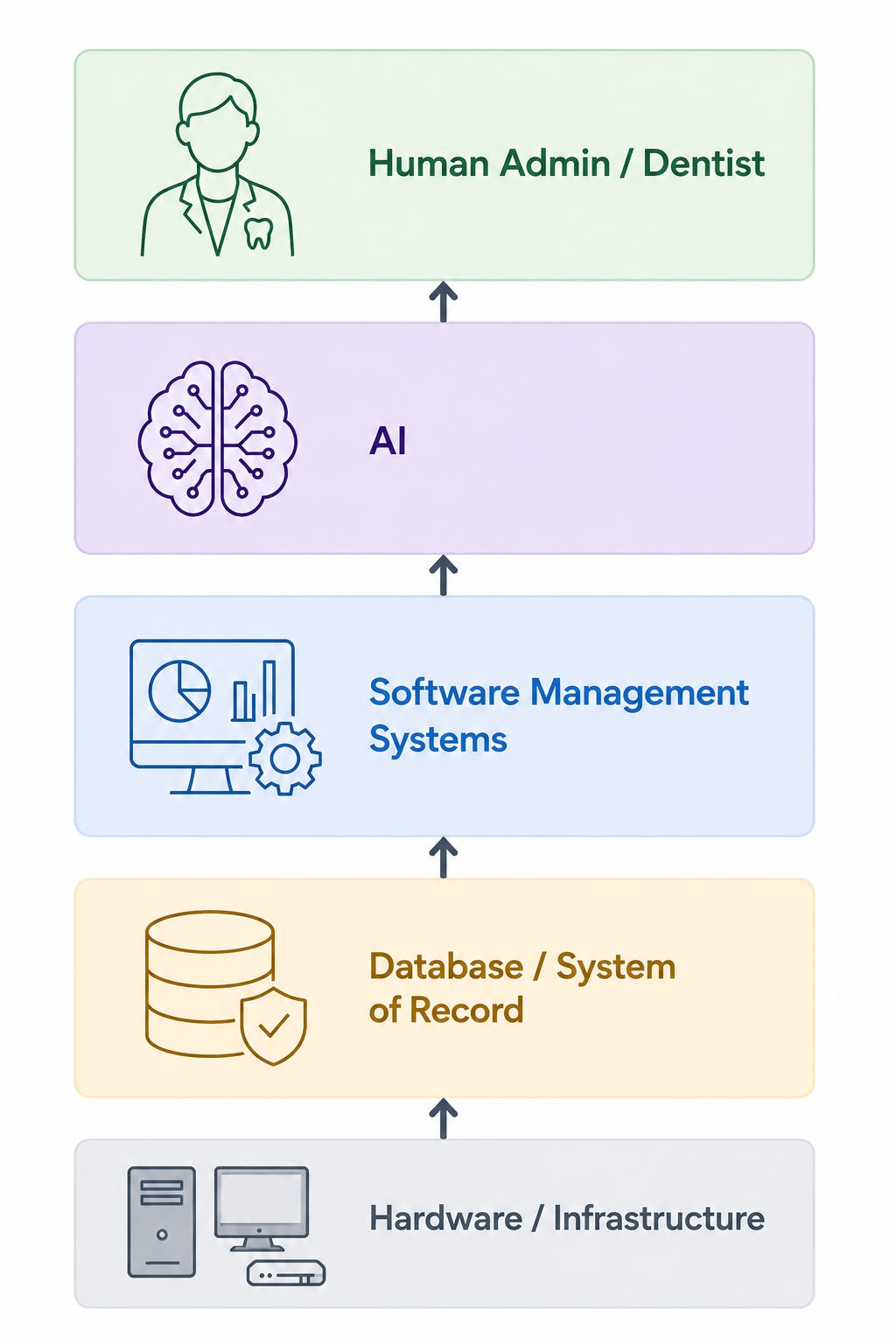

If I have ChatGPT try to draw the simple dentist tech stack, it’s like this:

Note there’s a little overlap between the software, AI, and human activities, and the economic value each one creates.

I’ve started looking at other industry verticals, and similar things seem to be happening. In municipal transit systems and such (which CSU owns several of), and automotive dealer management systems, most AI-native start-ups are building functions and agents that sit on top of the legacy vertical market software system and the database. They do not replace them. So the transit AI would try to do better route optimization and driver scheduling. The car dealership AI would book and confirm appointments with customers. Etc. But only in a very limited number of cases are they attempting to re-imagine and re-build the entire vertical market software system and the system of record (e.g., Tekion in car dealerships). They’re slotting themselves between the humans and the software+database. They automate some of human’s workflows and interact with the legacy software and database.

So none of this replaces CSU’s businesses or competes head-on against them.

But it probably will. Why?

Land and expand is a common phrase in the software business. In software, you get your foot in the door (“land”) with a basic package and core system you sell a new customer. Over time, you “expand.” You up-sell new modules to meet more needs and automate more workflows and such. Ideally, the customer is eventually buying many important things from you. You now have a deep, sticky relationship wherein you can keep up-selling new stuff and/or raising prices because it’s now hard to get rid of you (i.e., you have a moat, from “switching costs”). It’s then hard for competitors to conquer your customers.

Some of the above guys like Lassie will eventually get smarter. They won’t stop at 3-4 revenue cycle management things. They’ll look for more of what Susan does at the front desk, the layer above; and they’ll look at what the PMS is doing, the layer below. They’ll try to automate and sell what they can to the dentist as add-ons.

You saw: there’s money in it. We know there is an expanding economic pie. Before, Constellation could only help Susan fetch and enter data faster, and get her away from pen and paper and such 30 years ago. That was the $1,000/mo pie. Now there is the $500/mo pie Lassie is after. And Susan is still there, too, so there’s more pie left, more tasks to automate as you make Susan more efficient/productive, or redundant.

So, there’s a clear path and an economic incentive for Lassie et al. to encroach onto Constellation’s turf and/or into “white space” by automating Susan’s work. And that’ll happen across various industries.

So there’s a race to capture and/or maintain this pie.

And if this is the race Constellation and Lassie will get into, let’s run it and see. I don’t think it’s fair at all.

They start from different positions. Recall the tech stack image above. Lassie’s starting in the human/AI layer. Their economic incentive is to try and (a) capture more of that layer and (b) move down into the software and database layer and capture those economics, too, where they can. By contrast, Constellation is starting in the software & database layer, and their incentive is to defend this layer while moving up into the AI/human layer and capture the economics there.

Now, pick your horse. You can ride Lassie, or you can ride Constellation. Which do you choose?

I think Constellation has more structural advantages than Lassie.

Customer intimacy: CSU’s business units have known their customers for 10-30 years. They know everything the customer wants, and every new thing the customer wants or can get as technology slowly improves, too. Lassie doesn’t know nearly as much about its customers, which is why it doesn’t already have a deeper solution for them and just has a skin that does revenue cycle management.

Switching costs/incumbency: Lassie’s success shows you it’s quick and easy to sell a customer a solution to those particular workflows. You can onboard them in days. CSU’s VMS stickiness (low churn, high pricing power) and long onboarding times show its not quick and easy to onboard a new VMS to a customer. It’s very easy for CSU to move up a layer, and very hard for Lassie to move down a layer.

Financial capacity: CSU has significantly more financial resources and a far better understanding of what makes good returns on capital and what doesn’t, when it comes to different modules, how to market them, etc. If new features would have good economics, CSU already knows or will figure it out faster.

Local scale: in many cases, CSU owns the #1 or #2 competitor in its niches, and so has the best scale economics. It has more capacity to invest into R&D and sell it across more customers than new entrants. It could even cut pricing for a time to push them out, perhaps. (I’m less sure about this last bullet, to be fair.)

Negotiated low-cost agreements with the major models, so they can create and run AI features for cheaper than a start-up can. CSU pays less for the same thing so they have a unit cost advantage Lassie et al. can’t beat.

I think CSU is in a better spot to take Lassie’s economics, than Lassie taking CSU’s economics.

Look, obviously Constellation and Lassie aren’t really competing directly now or maybe ever, but the point is there are a thousand Lassies in the world now, across industries and countries. Many of those overlap with CSU’s 1,000 small VMS businesses. The point is…

They’re competing for the new economics and attacking each other similarly, and,

Constellation has the position, capacity, tools, and time to adapt and win.

My opinion, at least.

“Software will be free”

Anthropic CEO Dario Amodei said that. AI tokens will become so cheap, people will write software at almost no cost. That massive cost deflation means software can be priced very low and still be profitable to produce. It means there will be loads more software vendors in each market, and their collective rivalry means price competition. Which more of the economic benefits go to customers and not the software vendors.

To begin with, this isn’t playing out.

An AI-heavy VMS start-up, Tekion, is head-on attacking the likes of CDK, Reynolds and Reynolds, and other DMS like Constellation’s Auto-IT (maybe). They’re trying to re-create the entire DMS and system of record, while combining it with the CRM and other car dealership needs, and make it AI-native so you can talk to it and such.

First, to my knowledge, it’s premium-priced in the market and is expensive stuff. Its market positioning is that they do more for you, it’s integrated more seamlessly, etc., so you’re willing to pay more and buy additional modules, use more AI tokens, etc. Tekion is growing among Tier-1 dealers like Ford and BMW, but not among independent or used car dealers.

So the software isn’t free, and it isn’t competing on price.

And it certainly isn’t free to write. Tekion has needed to raise over $600 million in funding the last few years. It can’t all be for marketing: they have >1,300 engineers. If development is so cheap or easy to vibe-code, why are all these start-ups still hiring devs, who need to manage multiple AI agents, and such? It doesn’t seem like the cost structure for software has changed so much, so quickly.

To end out, when defending against AI-native start-ups, CSU has an extra advantage most other legacy software vendors don’t have.

CSU competes in super small end-markets, often under $100 million niches. Maybe even $10 million sometimes.

This doesn’t fit the entrepreneurship and venture model very well at all. The fact Tekion can afford to try and re-create the whole VMS with AI is because the end market is huge. Franchised (like Toyota) auto dealerships in the US alone do $1.3 trillion revenue. If these guys are spending 1% of revenue on a DMS, that’s a $13 billion end-market. It makes sense for Tekion investors to hand it some $10 million Series A money and start going after it, then some $200 million in Series B money and keep going. There’s potentially a huge payoff at the end of the endeavor.

That isn’t true, and doesn’t work, for some niche municipal tax system CSU provides to a few cities. You can’t even scale it because different cities tax differently, etc. Same with a traffic ticket system, etc. How do you convince VCs to give you $30 million to go after a $30 million end-market? Where is the big payoff for them? The juice isn’t worth the squeeze. VCs need a home run every now and then in order to make their investment model work, since most start-ups fail or turn into zombies. So they can only go after potential home-run opportunities.

Maybe guys like Roper Technologies will have to work a little harder to defend their turf. In many cases they have $1 billion end-markets. But most of CSU isn’t like this.

(Heck, 60% of CSU’s revenue isn’t even in the US. It’s in other countries with shallower venture capital systems, like Poland, Vietnam, Canada, etc.)

To wrap up, more evidence shows the market’s fear seems worse than economic reality. Our conviction grew a little and we bought more. It’s about the best risk/reward we have found among out current holdings and idea pipeline.

— Chris

wCash & leverage: the cash balance is going to decrease shortly as I zero out a loan within the family, at which point I will be 0% levered and hopefully have untapped leverage in the future if/when the market presents attractive opportunities. Historically, I have run my life with a modest amount of leverage, around 10-30%, whatever I could quickly pay back with salary over a few months. I don’t use margin loans since they’re callable. I borrow in other forms.

ICLR & SNX: Note ICON Plc and TD Synnex grew as a % of the portfolio, but we haven’t transacted. Both stocks have just ripped a lot lately. SNX CEO Patrick Zammit and his team have executed very well. Their Hyve subsidiary now does business with 5 major datacenter owners (“hyperscalers” like Amazon Web Services, Google Public Cloud & Gemini, xAI, Meta AI, and Microsoft Azure & Co-pilot), whereas they only had one or two of them when we first bought the stock. Hyve buys the parts through SNX’s distribution, helps design the server racks, assembles them, and then ships them to the data center site in big bubble wrapped boxes, ready for Azure’s contractors to set up. Unless you live under a rock, you know the AI datacenter business is growing rapidly. Meanwhile, the legacy SNX distribution business continues to do well given the demand for IT hardware in this investment cycle. The stock’s more than doubled to $280/share, 16x its $18/share earnings. We originally paid 6.7x earnings, which we felt was stupid for the scale leader in a scale business, where the industry was growing 5% annually, and SNX was positioned to potentially gain a lot more work through Hyve. We didn’t know it was going to happen, but we were getting all of Hyve for free, and the base business — the industry leader — at big discount.

ICON Plc turned out not to be doing anything fraudulent, as we thought. The business fundamentals also seem to be accelerating with strong new client bookings in the last 6 months. The stock’s now $158 vs. the $90 we paid, for something we thought did $10-13/share free cash flow (7-9x free cash flow), and would grow low or high single digit while earning 100% ROICs given its asset-light model. Alongside IQVIA, ICON is the industry’s scale leader as well and has one of the most diversified books of business among its biopharma clients.

We may own more CSU if/as I gain further evidence.

I took a crack at modeling Topicus (TOP), CSU’s partial spin-off, but didn’t find it nearly as cheap. It’s likely I’m wrong in that Topicus has a longer runway in Europe than CSU does with its North American tilt, but that’s not something I understand well enough yet, so I’m not confident paying for that assumption. Topicus’ industry diversification is also weaker. I’m OK if this one gets away from me.

I’m also learning about the IT consultants as a way to play AI-related misunderstandings, but I have more conviction in Constellation than I do in guys like Accenture (ACN). Quantitatively, CSU’s economics are slightly better, too, and it’s not much more expensive. Both companies’ tangible returns on capital in their core businesses are very, very high. Both have similar organic growth rates (ACN is maybe 1-2ppts better), but CSU has much higher returns on reinvested capital through M&A, and a higher reinvestment rate, so there’s far more value creation. It’s similar at CGI, Capgemini, and the like.

I agree with you that Constellation Software is a better investment than the IT consulting companies since it already has a large and sticky customer base, while consulting companies have to get contracts renewed with their clients and compete with each other.

Any thoughts on the payment sector? That sector is also getting beaten down this year like software.