Constellation Software (TSX: CSU) Report & Thesis

Bloodstained Stars

~35 min read. As usual, I recommend reading in-app. The email can get truncated, plus I may make edits after posting. (If we change the reports, we don’t edit. We post a new one. You can always audit our original thesis.)

We’ll cover our recent Constellation Software investment in more detail. The report’s attached at the start of the “Intro” section. This post will be a more accessible version of the report, hitting on the key points.

I swear every time I write these I get writer’s block several times and feel like:

Nevertheless, I hope you get something out of the investment idea. Judging by feedback, I’m harder on me than you guys are anyway, haha.

Before we start, is it happening? Maybe it’s happening. A friend sent me:

| Video gifs by quotes | 0603de39 | 紗")

Shoe company becomes GPUaaS company. Ok lol. This is like pre-COVID when companies became Bitcoin miners. Shiny object syndrome is running rampant.

Now we can start.

Today’s quote’s from Constellation’s indirect competitor, Roper Technologies:

“Once the company is part of Roper, we operate a decentralized environment so our businesses can compete and win based on customer intimacy. We coach our businesses on how to structurally improve their long-term and sustainable organic growth rates and underlying business quality. Second, we run a centralized process-driven capital deployment strategy that focuses in a deliberate and disciplined manner on cultivating, curating and acquiring the next great vertical market-leading business or tuck-in acquisition to add to our cash flow compounding flywheel. Taken together, we compound our cash flow over a long arc of time in the mid-teens area, meaning we double our cash flow every 5 years or so.”

— Neil Hunn, CEO, Roper Technologies

You’ll see this is not so different from Constellation.

Intro & Core Thesis

(VMS means vertical market software, which is specific to a niche sub-industry, like a subway system, forest logging operation, or car repair shop. This contrasts with horizontal software, which has use cases spanning many industries, like Microsoft Excel or Salesforce. Currency is USD unless stated. CSU’s reporting & functional currency is USD, not CAD.)

I won’t lie, this is/was a hard one, but I think my key conclusion is right:

CSU has both time and capacity to adapt. The management is more than capable of doing so.

Base case: if they continue navigating AI-based changes well, I think the stock’s worth USD 3,300 / CAD 4,500+ today (+60%). In 5 years, it may be earning USD 300 per share and be worth USD 8,000 per share (+180%), even if it’s less successful at M&A going forward than it has been in the past.

Downside case: If they don’t, I estimate that if 50% of their businesses go into structural decline (while they keep acquiring), there’s 20-30% downside from the CAD 2,400-2,900 we’d been paying.

We can do a 2x over 5 years even if the multiple never re-rated, because the underlying economic performance is so good. We can do a 3x if we are both right and the market starts paying a fair price for CSU’s economics. And if we screw up we should about 1x our money, walk away looking silly because we wasted time, but we’ll live to fight another day. Those characteristics fit squarely in our process.

As usual, I believe the weight of evidence thus far supports the base case and not the downside case, so we think the bet is mispriced and that’s why we bought.

Thus far I’ve taken a 5% position in the portfolio and continue to learn more about software.

Alright, what do we mean they have time & capacity to adapt?

(1) Time:

VMS vendors are deeply entrenched with customers and hard to rip out. I.e., competitive advantage is derived from high switching costs (plus a bit from hard-to-replicate intangible assets).

How?

One Constellation VMS will usually do many things for the customer, orchestrating multiple key workflows across business departments. It’s also the customer’s auditable database (“system of record” or “SOR”). Think about a car dealership customer’s repair appointment plus the technician’s matching work schedule plus the relevant part order and status, and all the associated records and costs, all connected to the company’s general ledger for accounting and tax, and even with integrations to the customer’s suppliers to order OEM parts, pass-through discounts, etc. They are using a Dealership Management System (DMS) to do all this, such as DIS, a Constellation subsidiary. Ripping out and replacing good DMS VMS is at best a 1.5 year project. It will cost several percentage points of revenue. It will take the IT people and management a lot of time and effort. Everyone at the company will need to be re-trained to learn it. They will probably have to run two DMS in parallel during the testing phase to ensure the new one works before unplugging the old one. There will probably be a consultant helping move data and do other parts of the implementation. The more software modules and functionality they bought from the vendor, especially customizations and integrations/APIs connecting to their other systems, the harder it will be and the longer it will take.

Meanwhile, VMS itself is a small cost. The license or subscription fees usually amount to 0.5-2% of each customer’s revenue, according to various sources. You also know it’s not material because I have never once in 15 years heard on a quarterly call or read in the MD&A: “XYZ software vendor raised their prices, so our margins contracted.” It doesn’t move the needle, so it’s not mentioned.

This low price vs. mission-critical importance means: unless your VMS has failed for years to keep up with your business needs, or unless the vendor is sun-setting the product, there’s no economic gain from switching VMS vendors. If you are a 20% margin business, your VMS costs 1% of revenue, and you somehow get a competing software vendor to offer 30% off… then whoopee, you are now a 20.3% margin business. Big deal. For just 0.3% of margin, you’re now jumping through many implementation hoops.

So, it’s far more important that your VMS performs the things you need to run your business.

This is why “change my core systems” is rarely in the top 10 of CEOs’ “important things to do in my 5-year Business Plan.” Unless your existing vendor is 10 years behind on features/capabilities, it’s just not worth switching.

Thus, customer churn rates on vertical market software can be 5% or less. For reference, that’s about how long people you know tend to stay with their primary bank (personally, I’ve been with TD since mom & dad got me a youth account in high school). By contrast, less embedded software like Slack/etc. has ~10% churn rates, while random “Joe Software” mobile apps and stuff may be 15%+. It’s harder for those guys to retain customers because the economic bond is much weaker.

This is also why good VMS vendors can raise prices. A 5% price increase on something that costs 1% of a customer’s revenue is 5 cents out of their $100 in revenue. It’s nothing. If you make the customer’s business even 5 cents more productive with improved features, it’s worth the increase. Even if it’s not justified that year, and the customer doesn’t like it, it still doesn’t make business sense to do anything about it. Recall the cost and disruption above, right? Ripping this stuff out is not usually justified.

So, the customer relationship is deep, and it’s very sticky.

This switching cost means when things are broken, or the world is changing and customer needs or solutions are changing, CSU has time to adapt to change because the customers can’t and won’t run away overnight, even if CSU is lagging behind.

(2) Capacity:

Take this in two sub-parts.

First, they’ve got the capabilities. Partly because they’re a bit weird.

Constellation is ultra-decentralized, kind of like Neil Hunn said about Roper above. But in their own way. (Founder Mark Leonard once said: “We are the anti-scale-of-economy company.”) This has some disadvantages, e.g., there are a ton of duplicate costs and it’s at least partly why CSU has among the lowest margins of any mature software business.

But there are advantages, too. CSU is big on autonomy, culturally. When they buy a subsidiary, the existing founder/CEO often stays on, more or less exchanging their stock for CSU stock in the collective company. CSU is organized in such a way that these founders have a lot of interaction with each other, and with customers, but each of them runs their own business unit independently. Multiply this by 1,000 VMS business units, and you should see it creates an absurd amount of institutional knowledge. If it was one big brain, CSU probably knows more about VMS and about its customers than anyone in the world. CSU often knows more about its customers’ needs than the customers themselves, such as regulatory reporting requirements, etc.

This puts the business unit managers and the executives front and center with respect to industry changes, including through the customer’s eyes.

Second, the opportunity is right there, and they arguably have the right to win it.

We always go back to (a) a company’s value proposition, and (b) its core activities which create that customer value.

What value does software add? What, specifically, do Constellation’s ~1,000 VMS subsidiaries do for customers?

Ask companies and read annual reports from the bottom-up. Or, from the top-down, look at country-level government data on corporate revenue, costs, and total wages. You will find: labor is typically the #1 cost item for many businesses, or at least top 3. (Another big one is materials; it varies by industry.) Many businesses spend more on rent/utilities and freight/logistics than on software.

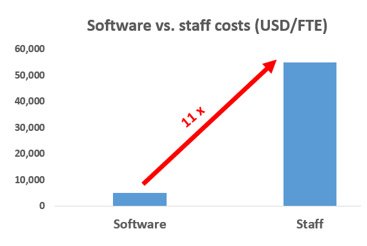

Now consider: VMS exists to create labor & production efficiencies, right? It attacks businesses revenue & cost items and helps digitize & standardize them, making businesses more productive. Most businesses have 5-20% operating margins, so good software has big benefits vs. the cost. Consider a professional services company like an engineering or IT consulting firm, with 20% margins. Most of the cost base is wages. If you could make people just 5% more productive by making their workflows easier, you can gain 4 percentage points of margin.1 4% of revenue is 4x what your core VMS costs.

Even today, in the US for example, the typical business spends ~10x more on staff per employee than software per employee:

If you agree that core business software helps make people and capital more productive (revenue per input, cost per output, etc.), then this tells you clearly there’s still a ton new & existing software can do to improve business workflows. We don’t know what all this “white space” is, but can see it’s there. A lot of it. And good VMS vendors like CSU are attacking it.

(Sorry, person, yes, you are expensive. Yes, software is trying to make you less expensive.)0

I think this will go to some kind of AI-enabled VMS, rather than pure-play LLMs, etc. It won’t be standalone AI.

Why?

Well there are obvious reasons, like the fact software is deterministic (i.e., the same input gives the same output). It makes business guardrails: it simplifies workflows into clear pre-defined steps that are consistent and meet some measurable standard that executives can track and work on improving. With LLMs, this is trickier because LLMs are inherently stochastic/probabilistic. Try it yourself. Give a foundation AI model the same inputs and you’ll get slightly different outputs from time to time. Last, it also takes a ton of compute on dedicated hardware (GPUs in a datacenter) to do that. Legacy VMS systems do more, more strictly, for less. So “strict” workflows will probably stay on legacy software and “contextual” stuff will go AI.

Less obviously, this means things will probably go hybrid because there’re both strict and contextual workflows in businesses. For example, hospital management and electronic medical records management VMS will go hybrid. A doctor will use an AI LLM to dictate and transcribe patients’ notes or document a procedure for patient & legal records. That’ll then sit in a legacy database attached to the patient record. To schedule the patient, reserve a bed, track their prescriptions, bill their insurer, schedule and pay staff, etc., will probably remain legacy software. But to assist doctors with judgments about what to do with patients, they’ll use AI to query these notes and the patient’s history, etc. So, for the VMS vendor to capture all the potential value-add with a hospital customer, they’ll need to implement some AI functionality alongside legacy systems.

If you look around, you’ll see a lot of existing software vendors already taking this approach. And you’ll see a lot of AI-native start-ups building deterministic software. The models are converging.

Constellation just has to see opportunities like “oh yeah, we can integrate the dictation into our existing hospital management system” and then do it. Because their culture facilitates the rapid-iterating, customer-oriented learning machine I described above, I think they will find things to do like this, in turn deepening the commercial relationships with customers and fending off competition.

Not to mention, they’ve got the existing knowledge base. Many of CSU’s business units have worked with the same customers for 20 years and know their businesses inside and out. This puts them in the best position to walk them into whatever new hybrid world comes; that’s a big barrier for start-ups, who not only need to figure out a lot from scratch to compete, but also learn just as much about the customer.

This institutional knowledge is a very valuable, very hard to replicate intangible asset. If you think this is woo-woo, I’ll give you an example. It’s kind of like Facebook’s or YouTube/Google’s so-called “Walled Gardens.” That’s all the data Facebook/Instagram have on 4 billion users around the world, with a ton of information on each person that lets them easily help advertisers target the consumer segments they want to target, with high precision, rather than imprecise, big-blast-radius advertising like the Superbowl or highway billboard or cable TV ad. That garden is paradise for advertisers, because they can put messages in front of exactly the people who’d be likely to buy, and get far higher return on ad spend. How does one learn as much about 4 billion people? How do you replicate Meta’s walled garden and compete with them for advertising dollars?

The inordinate amount of proprietary information 1,000 CSU founders know — and share with each other — about how software can solve customers’ needs… is a walled garden.

There is no new emerging competitor that can magically replicate this.

CSU is well-managed and isn’t sitting still. It is already doing a lot of this. Many of its business units have been testing and are now deploying and selling AI-enabled modules for certain workflows. Furthermore, the company has agreements with all the major LLM providers, which help it get lower unit costs per AI token at the datacenter, and get it help when customizing models. CSU is getting in front of the potential threat, using the tools it has at its disposal to turn some of that threat into opportunity.

CSU clearly has the capacity to adapt.

Combine this with the high switching costs that buy it time, and I think Constellation is positioned to do fine.

They have the capacity and the time to adapt.

That’s my thesis.

Summarize by going back into the customer’s shoes:

I am a car dealership CEO/owner (or whatever industry vertical).

I have a bunch of workflows at my business that need to be orchestrated while meeting some performance standards (otherwise I won’t have customers for long).

These are things like scheduling car repairs, technicians to do the repair, parts ordering, emailing the customer an appointment confirmation, invoicing/billing the customer, paying my technician the hours, journaling the entries onto my accounting ledger, and reporting the workflows so that I can track the company’s monthly operational & financial KPIs.

I have a VMS system that basically orchestrates all of this for a relatively low cost.

A new start-up comes in with “hey we have this cool AI model that optimizes your scheduling/calendar. It calculates the best weekly repair schedules and sends phone-/email-based notifications to your technicians, customers, etc.”

You think, “okay, cool, but how does it fit with all these other things I need to do?”

Even if it fits (has software integrations), it doesn’t replace those things.

So you still need your VMS.

At the same time, your existing VMS vendor is in a better position to build this calendarization if their current scheduling module isn’t good enough. They can just do that and not lose share of wallet in the future.

The start-up cannot go the other way: it’s way harder to replicate the whole dealership’s system of record, staffing and invoicing system, etc.

Even if they could go the other way, the system has to be significantly better in order to incentivize the dealership owner to switch. Otherwise, why are they going to embark on a 2-year implementation project and retrain all their staff etc.? If the VMS is decent already, there’s not enough impetus to switch.

Further, how will the new start-up make a better system if the incumbent guy is the one with 20 years of accumulated customer knowledge?

So the competition for customer wallet is very one-sided. If the VMS vendor is decent, they still win even if the new AI-native competitor is a genius.

The customer is most likely to stay with the VMS vendor long-term, and the VMS vendor is more likely to maintain & capture wallet share as long as they adapt.

This is why I think it’s going to be harder to displace good VMS than CSU’s stock price now implies.

Future Runway

Even if CSU isn’t displaced, the stock’s not super cheap.

The second lever is future M&A. For us to make money, CSU must also

(a) continue acquiring good VMS businesses, at

(b) attractive prices (~20% ROICs),

(c) at a good pace,

(d) for many years.

Sounds tricky. Can they? I think it’s reasonable to believe yes.

CSU owns ~1,000 vertical market software businesses already, acquiring them over the last >25 years. It will soon be doing USD 3 billion in free cash flow from these.

Yet the company’s actually not that big.

It turns out, there are something like 100,000 VMS businesses in the world, all solving big problems for niche customers at low cost. Think of how many logging companies there are, maintaining their forest inventory (logging logs and entering the data into their logs). Municipalities with public transit. Warehouse management. Fleet logistics. Truck repair shops & dealerships. Legal case management. Hospital management. Retail point-of-sale and ticketing systems. The stuff’s everywhere, once you notice.

CSU owns just ~1% of the world’s little specialist software companies. There are a ton left to buy, and there are maybe a handful of serious serial VMS acquirers out there (plus many smaller ones). Many of VMS companies’ founders don’t have a permanent home for their business when they want to sell/retire/etc. Also, many of these are only ~$5-50 million in revenue with a few tens of staff and a hundred customers. So they’re not easy to find, there are a ton of them, and there aren’t many good natural buyers for these businesses.

CSU has M&A people and relationship-builders everywhere (e.g., I know a CSU person who sources potential acquisitions in a small Southeast Asian country), and maintains a big CRM database of their deal pipeline, with “well over 50,000” targets in their database the last time I asked anyone a few years ago. They find new ones every year as software firms grow and digitize more and more of the world’s workflows. As far as I have been able to find, there is no other company on Earth that has CSU’s deal-sourcing engine, with hundreds of people going around the world and shaking hands, building relationships across a hundred thousand potential sellers. Others exist, like Banyan or Valsoft (private), but they don’t have anything like Constellation’s breadth & depth. For example, Descartes Systems (Canada, public) only focuses on logistics/transportation software and also makes changes after acquisition, integrating companies into its one big platform. Other acquirers are only regional and don’t have the same sourcing depth. Others, like Roper Technologies (US, public), have a different sourcing engine entirely, where Roper only buys larger VMS businesses in the ~$1 billion range, usually buying from private equity firms like Vista Partners and Thoma Bravo.

Nobody who has the financial and operational capability to buy 100 tiny software companies a year. It took CSU a long time to get the sauce just right.

Because this is so difficult, it’s also the least efficient part of the market. E.g., I estimate Roper is earning ~12% returns on capital on M&A buying medium-sized VMS companies from sophisticated sellers like Thoma Bravo.

By contrast, I estimate Constellation is earning ~20% returns on capital on M&A buying a tiny $20 million revenue software company in the Philippines or Poland or the UK. The sellers aren’t as financially sophisticated, nor are they purely financially motivated, and they don’t have as many options.

For example, a large software company can easily be sold to “absentee” institutional owners like a big family office or to a buy-fix-sell private equity firm. At smaller companies, the CEO and their key 2-3 people are the company. There’s no where near the same redundancy as a large company. Most buyers therefore don’t have the operational capability to buy it. For example, when CSU buys, the plan might be for the selling founder+CEO to retire in 2-3 years. A key employee is trained up to the founder’s level and run the show. This is easier at CSU: there are already 1,000 entrepreneurs running CSU companies available to mentor and coach. Hence CSU offers far more than just financial value, which other buyers don’t often have.

Remember also that these aren’t early-stage, monster-growth software start-ups either. Some of them have been solving the same workflows for the same customers (like insurance companies) for 25 years. There’s little market growth: not a lot of new customer opportunities or a lot of “revenue synergies” with other buyers (where some big company buys this small company for the executive relationships, then tries to cross-sell all the big company’s products to the customer). You can’t really do that here, so this class of buyers isn’t as interested, either. It’d be different if these were new-ish software companies with some novel way of doing things a big company could exploit. But this is old, boring VMS.

Nobody really wants (or can find) them. Just CSU and a few others. But when the founders sell, they want someone to take care of it (or even stay on board and use CSU as a platform for getting even better at what they do, without heavy-handed oversight).

So CSU gets deals on these assets, and shareholders get 20% returns on reinvestment.

Lastly, you get cash or stock for selling your business. A lot of sellers end up with a bunch of CSU stock one way or another. It has been a great wealth creator for them long-term, and will continue to be if CSU can keep buying assets at >20% rates of return. With other buyers, you don’t get this. Many, many CSU executives are founders that sold to CSU, stayed on board, and are now much wealthier. And CSU never forced them to run their company a certain way after buying.

Both sides get a great deal; not many other buyers have so good an offer.

Given CSU does USD 3 billion free cash flow before M&A, and assuming 1 VMS costs CSU on average $40 million enterprise value, they need to acquire 75 companies next year. In 5 years, maybe 100-150. In 10 years, maybe 200-300 annually. Over the next decade that implies they need to buy ~1,800 companies, or just 1.8% of the VMS vendors that exist today, not even counting undiscovered ones now maturing. That seems very achievable to me.

And as you can see, CSU has the capabilities to get it done. And they offer superior value to many entrepreneurs who want to sell and safeguard their business, their people, and their wealth, without even losing control of their life’s work.

People have been trying to copy CSU’s model for many years, and there are a couple more serial acquirers and holding companies every few years, but CSU has always been the farthest ahead, with the biggest distribution (deal sourcing) and the longest-standing reputation and model. Of everyone that’s copied them, nobody’s quite gotten it right, even executives that left CSU to try it themselves.

What’s the problem, then? How AI disrupts VMS

The core market concern, I believe, is that there are multiple ways AI can attack software vendors’ current economics and future market opportunity.

An obvious attack vector: New entrants create AI-native apps that solve the same or similar problems existing vendors solve, but better. Not all software firms are entrenched with their customers; their switching costs are low. A no-moat software business might be something like a calendar/scheduling app/tool. I use Google Calendar, but you might use Calendly to organize your schedule and send/receive proposed in-person or video meetings with people. Unless you live under a rock, you’ve probably seen an ad or heard of some new calendar app. It might for example re-jigger your meetings with your solo-work time blocks, etc., to optimize your upcoming week’s schedule. Among other things. I have seen at least 3 such start-ups. I do not see why some of them will not at least split the market going forward. What cards does a Calendly have up its sleeve except the obvious response its executives will think of: “guys, we need to add AI-based optimization features too, and fast.”

Even “moaty” software businesses are at risk of this. Say there are modules you haven’t developed yet but should be, or ones you did but are only loosely-attached features to the rest of the software suite you sell. Someone can now develop apps to solve those workflows much more cheaply than in the past.

It gets harder than this though. And I don’t think I’m catastrophizing.

A deeper attack vector: customers backward integrate into making tools themselves. So, the barrier to writing code to create tools is falling. If you’re super smart, you can also just create workflow tools without an AI-assisted developer environment at all. Some guys are making tools in Claude, which has no developer environment, really. They’re not even experienced software people who are using an assisted platform like Cursor, which writes code for them but then lets them see all the code and edit it easily, etc. I know guys that just have Claude do something like once a week and then they check it, and it takes something off their plate that used to take 2 hours a week to do. Like stock screening.

In other cases, I have seen business owners get tired of explaining something to developers, so they just pop up Claude, explain the workflow, the problem, and the solution they want, then tell them the data structure they use, etc., and tell Claude to create an app that completes this workflow. And away Claude goes. It’s probably mediocre, but for some small, irritating workflow, that’s fine. It’s now “reasonably solved” vs. paying a bunch of developers $50K to make some dashboard or something or other for you.

This has multiple implications. One is that software modules these people would have bought will no longer be purchased. Maybe some Salesforce CRM module you might have wanted just no longer makes sense. Or some developers you were going to retain for a small custom build. You’re just not going to buy that anymore, and you might figure it out yourself if you can do it fast enough. Or one of your intrepid employees will. With people and capabilities like that in your organization, maybe people will no longer spend a lot of time searching for a VMS that solves their problems.

That deflates the market opportunity for a lot of software, but doesn’t necessarily kill the core business. So their revenue will grow more slowly now.

Software is “land and expand”, right? You sell customers the cheap base product, then you gate the really good/new features. The customer might want realize some of those bells and whistles could really speed up their business processes, so once they get familiar with how your base package works, they come back next year and buy several modules. Perhaps less of that happens now.

Another example attack vector: Substitution threats from horizontal software and custom-built ERP.

Traditionally, the way software works over the business life-cycle is a little like: first, you are small and can’t afford anything, so you go with really basic horizontal software out-of-the-box, like Excel. Once your organization is larger and more complicated, you have more intricate needs. You can’t just have people doing spreadsheets for everything, so you buy a VMS to run your business, which does something like 80% of what you need, instead of the 50% Excel does, and you pay a higher price point. Later, when you’re a large organization, you hire someone like SAP who custom-builds enterprise resource planning and other software for you and helps maintain it. It’s extremely expensive but does everything you want, efficiently.

If guys like Microsoft can do an amazing job integrating Co-Pilot based AI swarms into Excel for a really low price, then maybe you can do a lot more customization in Excel, and achieve 70% of what you want instead of 50%. At that point, maybe you choose to delay buying a VMS, and CSU misses out on this opportunity. The same could happen on the high end if CSU lets its products stagnate and customers choose more quickly to go with full custom-builds, which CSU tends not to do (they help you save money by recycling and re-selling you code from another semi-custom build for another customer, thereby spreading the fixed cost of product development across more customers).

As you can see, many of these problems are a little difficult for a shareholder like us because they are not easy to monitor, measure, and quantify if/as they happen, too. This is what makes the bet tricky, I think.

There’s already evidence these are happening at least to some degree. People are certainly attempting them, and bragging about it on places like LinkedIn.

It kind of looks scary on the surface. Substitution threats. New entry threats. Backward integration threats from your own customers/buyers. If you look at the common thread, it is: “somehow another guy implements AI better than CSU does, where the customer wants it.” Yet we kind of showed above that there are unlikely to be many players on Earth that have the same level of customer intimacy as CSU, and that can share, test, and implement new software knowledge as fast, at least in VMS. It looks to us like CSU has the tools and the market position to be able to deal with these threats appropriately.

Historically, they already have the track record. There are examples of many CSU business units integrating cloud-based features and functionality as software moved from on-premise to cloud-based. There are other examples when the internet grew up and CSU businesses shifted from being fully customer-side to having online connectivity and features, etc. This just looks like another shift in what the products will be capable of, and it’s just on CSU to identify where it makes sense to add AI-improved features and sell them to the customer. They have said publicly they’re already doing this.

So I think it’s hard to believe the expected outcome is “this business is going into structural decline.” We will take the opposite side of the bet.

Lastly, be aware there are even more things unknowable at this time, some of which benefit and some of which would harm CSU. For example, none of these threats really solves for: what is the cost to maintain that product over time? The biggest thing longstanding software customers are paying for is maintenance: upgrades, new features, support, bug fixes, security issue fixes, minor customization, etc. Maybe someone can easily develop apps now using Lovable to vibe-code it for them. But how do they know the app is secure against hackers’ attacks, long-term? Especially when hackers’ methods improve. Or, how do they fix the code when they try to make changes but the AI doesn’t make them in quite the way they wanted? More and more natural-language prompts until the AI model finally gets it?

Or it could just be maintained by an experienced and skilled dev base, using AI-based tools for assistance and code generation, letting them think through the hard stuff.

Ultimately, in a given value chain, activities move toward the specialists, right? Real estate owners don’t design their buildings, that’s not their core activity or competency. Something similar should play out here, where this core activity stays in the hands of the guys who know how to make and maintain software-based automation tools. That’s my view.

Valuation

I looked back. I don’t think I’ve ever paid more than 12x stabilized free cash flow for a stock. At CAD 2,400-3,000 per share, we’ve been paying 11.5x-14.5x for this one, and believe an implied “fair” multiple is ~27x free cash flow or more, depending mainly on how much & quickly CSU keeps acquiring.

Am I losing my mind? Am I getting caught up in the fact everyone seems to be paying 25x for anything half-decent these days?

I argue some businesses are worth more than others. There’s no magic here: it’s because of superior economics. Everything maps cleanly back to returns on capital, growth, and reinvestment. (If it doesn’t, your financial modeling needs work.)

CSU is one of these. The company and its software subsidiaries have the following key economic drivers:

(1) No organic investment needs: last 5 years capital expenditures average only 0.6% of revenue. There is nothing to build to sell more software dollars. (Just sales & marketing expense.)

Working capital is also negative 19% of revenue. Software vendors are usually paid up front for services not yet rendered. E.g., you pay your quarterly SaaS/licence fee now, then use the software over the following quarter. Cash now, service/cost later. This is typically recorded as deferred revenue. They also defer many of their own costs. E.g., employees like devs and sales staff are the top cost, and are paid in arrears. Therefore, net working capital is actually a source of free cash flow as Constellation grows, and even helps it acquire more businesses faster. Most businesses must use cash flow to “build” working capital to grow. Think of a store that must be filled with shelves of inventory before it can sell anything. Or a manufacturer that must obtain and store both raw materials and “work in process” components, etc. Most companies must invest in working capital. Software companies instead generate working capital float from their buyers and suppliers.

(2) Organic growth: good software businesses have inflationary (or more) pricing power, raising prices 2-7% annually, which is the case at CSU. So long as it can stay reasonably competitive vs. other options, good VMS like Constellation’s is so sticky the company can reliably grow its top line just by raising prices, not necessarily selling a lot more (although it also tries to sell new modules).

(3) Excellent inorganic reinvestment rate & economics: this is the big one.

Constellation has retained nearly all its free cash flow in the last 5-10 years, with only token dividends. It plows this cash back into acquisitions, which I estimate earn 20%+ returns on capital. This is equivalent to us receiving a dividend, and then me having to find a 20% return opportunity. I have never been able to do this consistently. Yet CSU’s doing it for us. Furthermore, if you think the average investor deserves a 10% long-term return on equity investments (the cost of equity capital), then Constellation is reinvesting at twice the opportunity cost of capital. That means each dollar they are investing is worth $2 or more in market value. And they have historically reinvested 100% of the dollars they generate.

There are very, very few businesses on earth that can do this.2

There are two variables here you may have noticed:

(a) Return on reinvestment: what can you earn on that retained cash flow

(b) Reinvestment rate: what percentage of your free cash flow can you retain

The higher each of these numbers is, the more the business is worth because these numbers are literally, in plain English: (a) how much value can you create — what return on capital do you earn — when you invest, and (b) how much of that can you do?

At CSU, the returns are ~20%ish, and the reinvestment rate is 100% historically, in that they have kept pretty much every single dollar and compounded it for us. They only borrow a little bit of debt to do M&A.

OK, that was a philosophy-of-finance tangent, but it is to say that if you believe CSU can do this in the future, too, and you model it correctly, then the shorthand valuation metrics like P/E or P/FCF or P/S (price to sales or revenue) should be a lot higher than most businesses, who cannot do this.

In my own valuation, which you can find in the report, I assume:

(1) Base case (2-3x over 5 yrs): CSU can only reinvest 60% of cash flow going forward, declining each year. The rest must be paid out to us, implying a lot less future value creation. I also assume the returns on reinvestment fall a little each year as good deals become harder to come by, implying the runway ahead isn’t as long as we might think. Lastly, I assume ~2.5% organic, driven by price increases, plus new modules, minus old module attrition, minus customer attrition.3

(2) Downside case (-20-30%): I assume a 50% reinvestment rate here instead. The big one is that I assume significantly higher customer churn as customers attrite toward some oncoming wave of new AI-native competitors, or toward better-performing horizontal software (say MS Excel magically becomes 10x more capable when a swarm of AI agents can rapidly build you some really spiffy stuff, and now you no longer need customized VMS). So I assume organic growth of -2%, which assumes some price increases and new modules, but that roughly half CSU’s businesses go into structural decline with high customer churn. I assume 5% terminal declines.

— Chris

Obviously the second-order effect here is that everyone is going to do it, then pass through some or much of the benefit to customers in terms of higher quality and/or lower cost products & services, but that still means everyone has to implement these productivity tools just to keep up with competitors. That’s the forced improvement from capitalism.

Take Brookfield’s subsidiary Brookfield Asset Management (BAM), the investment manager. It earns 50% returns on capital, however, that’s because it doesn’t need any capital investment: it’s just smart guys acting on investment ideas and charging fees + carry from clients for it. The capital really belongs to the clients. There is no where for BAM to reinvest. They dividend it up to the parent company, who must instead invest in more capital-heavy assets like ports and office buildings and solar plants and datacenters, which earn 10-20% returns on capital. Usually they’re just investing with the clients as there’s nothing better to do with the cash. Ideally, you want BAM retain the cash flow and reinvest it at 50% for you — wouldn’t that be something — but there’s no where to put it. That’s the problem with high-ROIC businesses; they don’t need capital. It’s usually why they’re so high-ROIC in the first place.

By contrast, CSU has a bit more opportunity to retain cash and put it to work buying niche VMS that not many guys want or can handle properly, and they’ve been able to make >20% doing it. That’s much better than paying dividends to us.

It is arguably a little low because of a “mix” effect wherein many of their businesses are transitioning to SaaS from licence & maintenance, which tends to depress organic growth rates at software companies, but Constellation isn’t growing net customers/seats very quickly like most software firms, and the rate of SaaS adoption is also much slower than most software firms, so the effect is probably much, much smaller than others like Adobe and Autodesk etc., have talked about.

Great post. Only one note: I think a combination of higher interest rates compared to the ZIRP era, as well as all the leveraged buyouts and software rollouts made by both private and public companies are now hitting the refinancing periods. Many will be forced to stop the "empire building" and sell off the businesses to pay off the debt walls. CSU will be in the first line to keep acquiring these businesses, and I think they'll be able to keep doing this for a little longer without needing to return the capital to the shareholders. I remember reading in one of the transcripts that they were lamenting low interest rates because most companies were not willing to sell at their required hurdle rates. It's true that they're growing bigger, but so far they've managed to grow despite an unfavourable macro environment, and the tide is shifting in their favour now.

I think the AI fears will also keep depressing SaaS prices, as any new model released will show more capabilities than the existing ones. As a net buyer of SaaS, this is good for CSU, because as you've said ultimately building and maintaining software is a liability, and nobody wants to wake up at 3am to fix their software because of an issue with a 3rd party API that broke backwards compatibility. This is true today and will remain true in the future.